Money

ANALYSIS: Facebook Is Kicking The Sh*t Out Of SNAP

Five years ago, Snapchat was the hottest thing around, more popular among users than social media kins Facebook and Instagram.

These days? Not, so much.

For one, since last year’s IPO—then labeled “one of biggest Wall Street flops“—the stock’s been dropping like crazy.

sooo does anyone else not open Snapchat anymore? Or is it just me… ugh this is so sad.

— Kylie Jenner (@KylieJenner) February 21, 2018

Since February, around the time a single Kylie Jenner tweet wiped out $1.3B in company value, Snap has dropped from a public valuation of $24B to $14B.

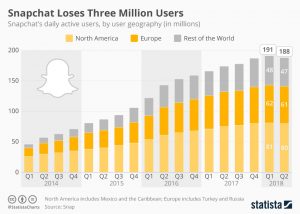

And get this: According to its Q2 report, Snap users are dropping like flies. Since Q1, a whopping 3M users have ditched Snap—the first time user count has dropped quarter-over-quarter in the company’s history.

And yes, Facebook has taken some legal hits lately, but Snap could be facing a battle much bigger.

If you can’t buy ’em, steal ’em (their users, that is)

While users are dropping en masse, Snap still sports a robust 188M daily user base. But competition from rivals is getting more intense by the day.

Facebook—who actually tried to buy Snap for $3B in 2013—saw its user base increase to 1.47 billion over the same period.

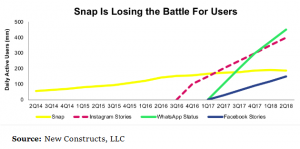

And powered in large part by their Snapchat story clone Instagram Stories, Instagram has grown to 400M users—more than double Snap’s user count.

Oh, it gets worse.

WhatsApp, another Facebook property, has their own version of Snapchat’s major value prop (WhatsApp Status), leaving you wondering exactly what Snap has to offer.

Users could be wondering the same.

For whatever it’s worth, while Snap’s user count has eroded, WhatsApp has seen a healthy spike in active users, peaking at nearly 450M.

Facebook Stories (at this stage, you get the point) boasts of over 150M users, as well.

When the decline began…

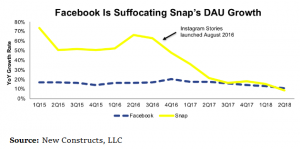

In the chart, we can see that Snap’s user growth has been severely impacted post the release of Instagram Stories two years ago. While Snap’s daily active users (DAU) rose 48% year-over-year in 2016, it fell to 18% towards the end of 2017. An extremely telling blow.

But it’s not just Zuckerberg…

From a business model standpoint, Snap is similar to the other internet blue-chippers (think Facebook, Google, Twitter, etc.). Their revenue is pretty much all advertising income; a total of 97% in 2017.

But that’s pretty much where the comparison ends. Unlike the other tech giants, Snap must be thinking they’re Big Meech or Larry Hoover, because they are blowing money fast.

Compared to Facebook, Twitter and Google—which have gross margins of 85%, 67%, and 57%, respectively—Snap has a paltry gross margin of 20%.

No way?

Yes way. Snap’s expected to continue to post negative margins in the short term. And they will need to figure out how to boost their average revenue per user (ARPU) substantially if they even want to think about being profitable.

Initially billed as the new Facebook, Snap has pretty much struggled to keep up according to every relevant metric since its IPO.

Facebook, on the other hand? Sure, they had a rough start when they debuted on Wall Street in 2012. But since then, Facebook’s enjoying healthy profits, racking in billions of dollars after tax.

And more importantly, Facebook’s market value has 10X’d, jumping from a $50.92B low to $520B as of Aug. 31, 2018. (They’ve been as high as $615B on July 16.)

So what can Snap do?!

Hard to say. It’s not just Facebook that’s kicking Snap’s rear end. They’re also way behind Twitter in terms of profitability.

In order for Snap to catch up with Twitter’s current growth, Snap will have to increase annual revenue by 46%.

Snap reports its first decline in daily active users, becoming the latest social-media company to post disappointing user growth https://t.co/u5KKslz0fk

— The Wall Street Journal (@WSJ) August 7, 2018

Facebook recovered after a rough start, why won’t Snap?

Well, in theory they could. Facebook did, right? And Facebook’s first few years were much worse.

Valid point, yes. But a couple of key points to consider. For one, Facebook was already the most sought-after social media platform when it went public. That wasn’t really the case with Snap.

And secondly, in order to achieve robust revenue growth, Snap will have to gain market share from Facebook—basically steal its users back. And at this point, that looks almost impossible.

But crazier things have happened. Snap away, WealthGANG…

Airbnb Experiences: 5 Easy Ways To Make Extra Cash Today

Airbnb is a great way to earn money by renting out your home or apartment.

However, did you know that you can also make money by offering experiences on Airbnb? Here are five easy ways to make extra cash today by creating and offering Airbnb experiences.

1. Offer a food tour

If you love food, why not share your passion with others? Create a food tour experience in your city, showcasing the best local cuisine. You can offer a walking tour or a bike tour, and include stops at local markets, restaurants, and cafes. This is a great way to meet new people and earn money at the same time.

2. Teach a skill or hobby

Do you have a skill or hobby that you’re passionate about? Share your knowledge with others by offering an experience on Airbnb. You can teach anything from photography to cooking to yoga. People are always looking for new experiences, and they’re willing to pay for them.

3. Host a cultural event

If you come from a different culture, why not share it with others? Host a cultural event, such as a traditional dance, music, or art class. This is a great way to showcase your culture and make some extra cash.

4. Offer a nature experience

If you live in a beautiful area, offer a nature experience on Airbnb. You can offer a hiking tour, a kayaking trip, or a birdwatching tour. People love to get out into nature, and they’re willing to pay for it.

5. Host a wellness retreat

If you’re passionate about wellness, why not host a retreat? You can offer yoga classes, meditation sessions, and healthy meals. This is a great way to help people relax and recharge, while earning some extra cash.

In conclusion, offering experiences on Airbnb is a great way to make some extra cash. With these five easy ideas, you can get started today.

For more ideas and tips on how to make money, check out this Airbnb guide inside our academy.

If you’re an Airbnb host looking to increase your revenue, there are several strategies you can implement to make your listing more appealing to potential guests.

Here are 10 tips for making more money with your Airbnb listing:

- Set competitive pricing: Research the prices of similar listings in your area to ensure you’re offering a competitive rate. Consider lowering your prices during slow seasons or offering discounts for longer stays.

- Offer extra amenities: Providing extra amenities, such as a pool, hot tub, or complimentary breakfast, can make your listing more attractive to guests and justify a higher price.

- Invest in high-quality photos: High-quality photos of your space can make a big difference in how many bookings you receive. Consider hiring a professional photographer to capture the best aspects of your listing.

- Keep your listing up to date: Make sure your listing accurately reflects the current state of your property. Update your photos, descriptions, and amenities regularly to keep your listing relevant and appealing.

- Respond promptly to inquiries: Quick responses to guest inquiries can lead to more bookings and positive reviews. Make sure to check your messages frequently and respond as soon as possible.

- Provide excellent customer service: Going above and beyond for your guests can lead to positive reviews and repeat bookings. Make sure to communicate clearly and address any issues promptly.

- Offer local recommendations: Providing guests with recommendations for local restaurants, attractions, and activities can enhance their experience and justify a higher price for your listing.

- Allow instant bookings: Allowing guests to book instantly can make your listing more appealing to those who need to book at the last minute. However, make sure to set clear guidelines for instant bookings to avoid any issues.

- Offer discounts for repeat guests: Offering discounts to guests who have stayed with you in the past can encourage repeat bookings and increase your revenue over time.

- Keep your space clean and well-maintained: A clean and well-maintained space can lead to positive reviews and repeat bookings. Make sure to keep your space clean and address any maintenance issues promptly.

Implementing these 10 tips can help you make more money with your Airbnb listing and improve your overall hosting experience. Happy hosting!

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login