Real Estate Investing

Real Estate Rockstars: 5 Millennial Realtors Who Are Crushing It In 2018

Housing sales dipped dramatically after the mortgage nightmare in 2008. But since 2011, the numbers have shot back up.

In 2017, 614,000 houses were sold in the U.S. In total, US real estate transaction volume hit $467B in 2017. But who are some of the hottest young agents brokering these deals? Here are five of the top realtors under 35.

1. Ryan Serhant

The NYC-based power broker and author of the bestseller “Sell It Like Serhant” closed deals that topped $838M last year. Ryan has built one of New York’s top real estate firms, raking in millions every year.

He initially entered the housing market in 2008, when the real estate space was seeing one of its biggest collapse. In his first year, he made just about $9,000 and decided to stick it out through the hurdles that came his way.

“Never in my wildest dreams did I think that 10 years later I would do [$100 million] in deals over spotty Wi-Fi while on a safari in South Africa like I did last week,” he told CNBC in April.

2. Blair Brandt

Blair Brandt is a 2011 Forbes 30 Under 30 entrant who rose to notoriety at 23.

Brandt’s company, The Next Step Realty, focuses largely on recent college grads.

“It’s been a total mess for young people who are graduating and moving to big cities to meet the right broker, to take care of it quickly, and to do it affordably,” Brandt told Forbes.

He matches recent college graduates with local realtors to help them find their first post-college apartment—and usually at a discount.

They offer discounted student brokerage fees, and hyper-localizes their experience by connecting them to a local broker to ease the process.

3. Jon Tetrault

Jon Tetrault and his partner at Slocum Realty snagged deals worth $24M last year and over $13M till date this year.

For the rising realtor, his success largely hinged on networking and sheer hard work.

“Always talk to people, and if that doesn’t work, talk to more people. Real estate is about building connections because that is what drives referrals. Research your region and look for the local chamber of commerce or any volunteer boards that you can join—these are all great opportunities to expand your network,” he says.

“Put yourself in front of people. Listen to other agents and what they say, jump in their car when they go to appointments. When you’re first starting out, you can learn so much from the stories and experiences of veteran realtors,” he tells us.

4. Oren Alexander & Tal Alexander

The brothers, who are with Douglas Elliman, have won over some of the biggest clients across the globe. Much to their credit, the team sold a modern townhouse in New York for a whopping $100M–a sale pitched as the priciest ever in New York’s history of commercial townhouse sales.

Oren and Tal also closed the deal for Miami’s most expensive mansion, apart from handling a string of other high-end, ultra-luxury sales.

5. Brian Erhahon

This young London-born rockstar barely has hit 30 (he’s 29), but he’s already running a 275-agent team. Working out Tustin, CA, Brian’s team has a transaction volume of $187.6M. He also recently earned a spot on Realtor Magazine’s 2018 list of 30 Under 30 Honorees.

In a competitive, cutthroat business, Brian has a unique spin on doing business. When he does events, all agents are welcome—even from competing companies, which draw up to 200 attendees. “We’re open and transparent and just like to collaborate,” Erhahon told Realtor Magazine.

By Sheryl Chapman

As we all know, the economy can be unpredictable at times. Recession is a common phenomenon that can affect the investments in your portfolio.

But don’t worry, there are some sectors that are likely to perform well—even during a recession. Here are five recession-proof investments that you can consider adding to your portfolio.

(Editor’s note***********:************ If you wanna learn how to start investing for retirement, check out the free lessons inside the academy! 📺)*

1. Consumer staples

Consumer staples are products that are essential to our daily lives, such as food, household goods, and personal care items.

These products are in constant demand, regardless of the economic climate. Companies that produce these items, such as Procter & Gamble and Coca-Cola, are considered recession-proof investments.

These companies have a stable revenue stream that can weather economic downturns.

2. Utilities

Utilities are another recession-resistant investment. People need electricity, gas, and water, regardless of the state of the economy.

Utility companies, such as Duke Energy and American Electric Power, have a steady stream of revenue and provide investors with a reliable source of income.

3. Healthcare

The healthcare industry is recession-proof because it provides essential services that people cannot do without. Companies that provide healthcare services or products, such as Johnson & Johnson and UnitedHealth Group, are likely to remain profitable during a recession.

4. Gold

Gold is a safe-haven investment that many investors turn to during times of economic uncertainty. Gold prices tend to rise during recessions because it is seen as a store of value. Investors can buy physical gold, gold ETFs, or invest in gold mining stocks.

GUIDE: 3 Ways To Invest In Gold In 3 Minutes Or Less 🔑📲

5. Treasury bonds

Treasury bonds are considered to be one of the safest investments during a recession.

These bonds are issued by the US government and are backed by the full faith and credit of the government. Treasury bonds provide a fixed income and are considered to be a low-risk investment.

In conclusion, these five investments are considered to be recession-proof because they provide essential products or services that people cannot do without.

Adding these investments to your portfolio can provide stability during times of economic uncertainty.

Airbnb has revolutionized the travel industry by providing an affordable and unique way for travelers to experience different destinations.

With over 7 million listings worldwide, it’s safe to say that Airbnb has become one of the most popular ways for travelers to find lodging.

However, as a host, one of the most challenging decisions you’ll face is determining the right price for your listing.

Pricing your Airbnb listing correctly is critical to your success as a host, as it can make or break your profitability.

Here are some tips to help you price your Airbnb listing for maximum profit:

Know Your Market

Before you set your price, it’s essential to research the market in your area. Look at other listings in your neighborhood, paying attention to the size of the property, amenities, and location. Check the availability of your competitors and the average price they charge. This information will help you determine your pricing strategy and ensure that your listing is competitive.

Consider Seasonal Demand

Seasonal demand plays a significant role in the pricing of your Airbnb listing. During peak seasons, such as holidays, festivals, and major events, you can charge higher rates. Conversely, during low seasons, you’ll need to lower your prices to attract guests. Keep track of events happening in your area and adjust your prices accordingly.

Offer Discounts

Offering discounts is an effective way to attract guests and increase your occupancy rate. Consider offering discounts for extended stays, early bookings, or last-minute reservations. You can also offer discounts to guests who leave a positive review or refer new guests to your listing.

Calculate Your Costs

To ensure that your pricing strategy is profitable, you need to calculate your costs. Take into account expenses such as cleaning fees, utilities, maintenance, and taxes. Factor in your time and effort as well. Your goal is to set a price that will cover all your costs while still allowing you to make a profit.

Be Flexible

Finally, be flexible with your pricing strategy. Test different prices and see how they affect your occupancy rate and profitability. Monitor your competition regularly and adjust your prices accordingly. Remember that the market is constantly changing, and your pricing strategy needs to adapt to stay competitive.

In conclusion, pricing your Airbnb listing for maximum profit is a crucial aspect of your success as a host. By researching your market, considering seasonal demand, offering discounts, calculating your costs, and being flexible, you can set the right price for your listing and maximize your profitability.

Happy hosting!

5 REITs that own iconic buildings you can buy today

Real Estate Investment Trusts (REITs) are companies that own and operate income-generating real estate properties.

Investing in REITs has become an increasingly popular way to own a piece of the real estate market without having to buy individual properties.

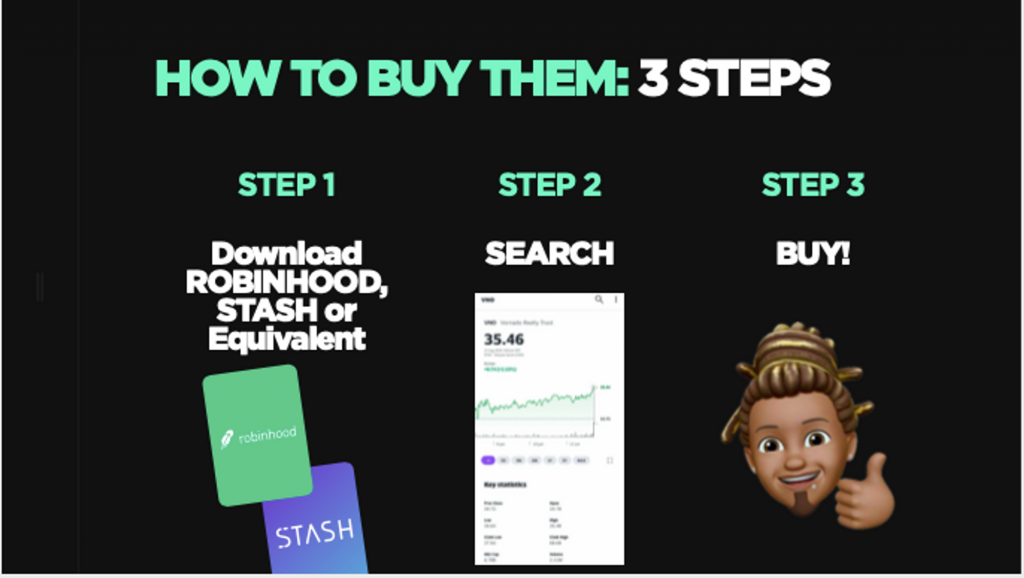

And you can buy them in the next 5 minutes on the NYCE app…with $5 or less.

Here are five REITs that own iconic buildings across the United States that you can invest in today:

- Empire State Realty Trust, Inc. (ESRT) – ESRT owns the famous Empire State Building in New York City, as well as several other properties in the city.

- Vornado Realty Trust (VNO) – VNO owns the iconic 555 California Street building in San Francisco, which was once the tallest building on the West Coast.

- Boston Properties, Inc. (BXP) – BXP owns several iconic buildings in the United States, including the John Hancock Tower in Boston and the Salesforce Tower in San Francisco.

- SL Green Realty Corp. (SLG) – SLG owns several iconic properties in New York City, including One Vanderbilt, which is currently the fourth-tallest building in the city.

- Macerich Company (MAC) – MAC owns several high-end shopping centers across the United States, including the iconic Santa Monica Place in California.

************************************************************************************************LEARN: How to own real estate with $1000 or less.

Investing in REITs can provide diversification and potentially higher returns than investing in individual properties. However, as with any investment, it is important to do your research and understand the risks involved.

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login