Business

Alternative Financing And Why Equity Financing Has Lost Its Luste

When a startup founder is ready to transform their idea into a viable business, they almost always look to equity financing–whether that’s in the form of checks from friends and family, an angel syndicate, or in rare cases, a early stage Venture Capital fund. This thought process is justified. In the embryonic stage of the startup lifecycle, exchanging equity for capital is often the only legitimate option to amass enough cash reserves to build an initial team, create an MVP, and hit the market, as debt investors will want security over non-existent assets and personal loans/credit cards can quickly become dangerous liabilities. Equity financing is also a proven (and expected) option for creating runway and providing growth capital for business expansion through a potential IPO or acquisition.

However, equity financing has its weaknesses–dilution of ownership stake, relinquishing board seats and autonomy of decision making, and irrational growth expectations, amongst others–and make raising a follow-on, or even first-time round less appealing to entrepreneurs who have creatively bootstrapped their way to post-revenue status. Every founder feels protective over their startup baby, and the thought of having a “growth at all costs” investor take over the helm is irksome. Removing the vagaries and potential biases of founders’ opinions, it’s an industry truism that only a fraction of startups looking to attain equity funding will ever achieve that goal.

Just this month, well known venture industry and NYT reporter Erin Griffith published an excellent op-ed analyzing the growing founder malaise towards traditional VC fundraising and the potential pitfalls of taking on equity financing when it’s not the appropriate long-term option. In the piece, venture capitalist Josh Koppelman of First Round Capital candidly remarks, “I sell jet fuel, and some people don’t want to build a jet.” Everyone knows what happens when you put potent jet fuel in a slow but steady single-engine prop plane—it stalls out and explodes.

Fortunately, alternatives have emerged to dislodge the binary outcome of either banking VC jet fuel or sputtering out entirely. This piece will shed light on the other financial options.. These providers have emerged to both complement and supplement the old guard of financiers, with most focused on helping post-launch startups meet short- to mid-term cash flow needs—without injecting so much capital as to force their trajectories towards the sun (or seabed). The advent of the cable car did not kill off transportation by horse—it simply served as a flexible alternative to meet local demand. Much like a startup idea, it was edgy, scalable, and pragmatic. Alternative financing upstarts today provide flexible, non-dilutive financing to entrepreneurs whose capital needs are not met by a time-consuming equity fundraise or difficult-to-obtain and restrictive institutional debt financing.

Breaking down alternative financing options for the startup economy (what’s alternative financing, anyways?)

Alternative financing is an umbrella categorization of non-standard financing solutions to supplement plain vanilla equity and institutional debt. For the startup economy, these solutions range from the more traditional: term loans, lines of credit, asset-backed loans, convertible debt, receivables/payables financing to the more creative: hybrid equity funding invoice/SaaS factoring, crowdfunding, microloans, grants/tax credit financing, revenue-share agreements, to the “wild west” of fundraising instruments–crypto/tokens.

Why so many options? If the demand is there, you better believe a savvy capital provider will attempt to manufacture a solution. Plus, the more arcane the structure, the lower the initial competition, and the higher the margins and ability to grab market share. These solutions are not only rising in popularity and easier to obtain, they’re also well-suited for the “torso” of the market—companies with varying levels of traction, a proven user acquisition strategy, and a readiness to grease the wheels on the marketing machine.

Flexible Financing to Drive Growth Without Dilution

When it comes to early- to mid-stage startups, some customizable financing instruments have emerged as clear winners in a competitive market where flexibility is the ultimate selling point. In addition to an emphasis on ease of use, the demand for many of these offerings is spiking thanks to quick access to liquidity and an a la carte menu of fee structures to decide between, from interest rates to transaction fees to revenue share agreements.

This is a unique segment of the market, where high growth rates and monthly revenue volume upwards of $500k-$2m remains unattractive to institutional banks offering single-digit APR debt. While $24 million a year in revenue might seem impressive, a revolving line of credit or an AR line on that sum at 8%/yr will gross just $192,000 prior to cost of capital, which could wipe out at least 50% of that margin. Again, low six figure fees might appear attractive to your average “Joey finance,” but they’re nothing for abank turning billions in volume a year.

In our overextended bull market where cash seems to be omnipresent, here are four of the most prevalent alternative financing categories providing liquidity geared towards growth, without the friction points of traditional debt and equity instruments.

Yes, you read that right.

If there’s anything the pandemic taught us, it’s that the paradigm of “office” and “workspace” has been shaken to its CORE.

Universities are teaching via Zoom, court dates are done virtually, FULLY REMOTE businesses are valued at $1B+, and legitimate Inc. 5000 startups are run from…wherever. 📲

This is my office for the day…

I am actually running our business from the beach, typing this from here.

It’s 4:28 pm CET, which means it’s 10:28 am EST and I am CRUSHING my to-do list.

(And the team will continue to crush it while I’m asleep. That’s the 🗝)

So how did we get here?

We launched NYCE and our mission to create 100,000 millionaires in March, 2020…just as the global COVID-19 lockdown happened. 😳

As a result, we shut down our main office and set EVERYTHING up to run remotely…

SMOOTHLY! And a system that allows us to outperform competition by 200%. (You can build this system, too. More on this in a second.)

Here’s what we were able to do since then:

- Gained 6M+ followers across all platforms 📈

- Add 1500+ new apartments to the portfolio 🤑

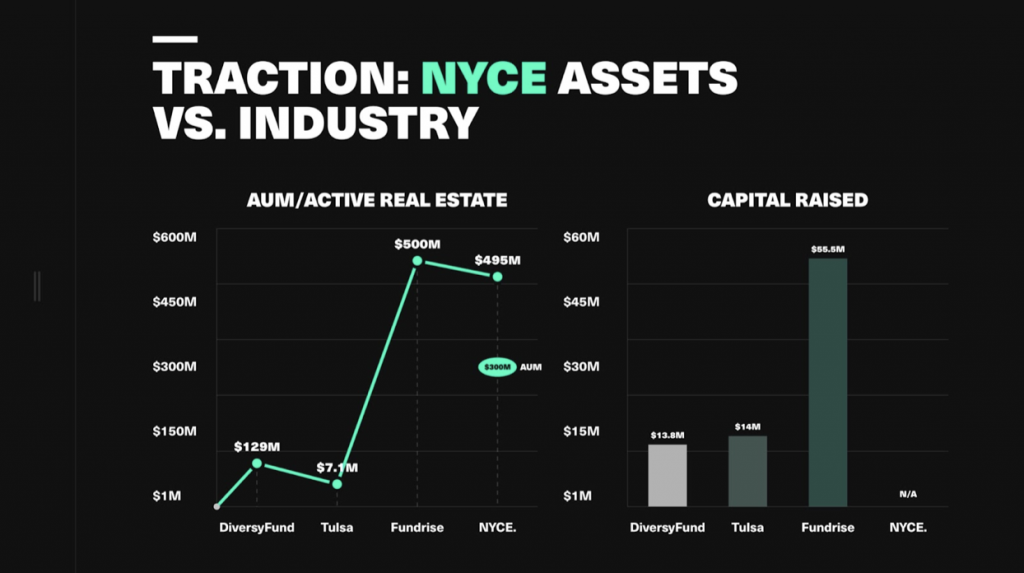

- Grow to $300M in real estate 🚀

- 105% investor returns 🎉

- 700K+ community members 🤝

And here’s the best part…

Having team members in all the main time zones gives us a 24-hour work cycle vs. 9-5/eight-hour on-the-clock performance.

This means we get 3x the productivity of a similar company. 🔥

Let me repeat that…3x PRODUCTIVITY vs. our competitors.

Meanwhile our project management software grants us 24-hour TEAM-WIDE connectivity that tracks all tasks and lets us know if productivity dips even a little bit.

There is ALWAYS someone senior awake. It could be Martin in Barcelona…Nat in New York…Vineet & Arif in New Delhi.

All the while giving YOU GUYS wealth hacks and daily content. 🔥

OK, so how can you do it?!

Well, the first step is to have an actual side hustle you’re launching. Not just an idea, a validated business.

MAJOR KEY: Do NOT spend money until you’ve made your FIRST DOLLAR! 🗝🗝🗝🗝

(You can catch a replay Business Launch masterclass here and see TRIBE member Nessa launched her business on the spot and got her first $45K client shortly after.)

One of the easiest ways to start is with Airbnb—you can start that in 10 minutes. Literally. (Here’s a guide if you need it.)

Once you have your business, you build a virtual infrastructure (you really just need two softwares, which are FREE), manage the team accordingly and run the business from there.

I’m gonna put together a step-by-step video breakdown this weekend inside the new TRIBE U on the FIVE key things you need to do this for YOURSELF. 💵 💎

From what software to use, how to build a team, how to keep.

In the meantime, drop a comment if you’re ready to build some wealth and any questions if you want more…

Let’s get to work. 🙌

PS: If you can’t be bothered with video and just wanna get to work, we’re hosting a TRIBE U workshop that will help you get this process started on the spot. It’s $479 $49. 🔥

Investor and popular Instagram influencer Philip Michael says new fintechs need to take greater responsibility for their younger traders.

“Promoting financial literacy is a must, but encouraging risky gambling is reckless,” Philip Michael, NYCE CEO, says.

In 2020, a 20-year-old Robinhood trader killed himself after engaging in risky options trading and seeing his balance $730,000 in the red, leading to a wrongful death lawsuit against the investment app.

“The main apps onboard as many new users as humanly possible, but there’s really no educational process,” Michael says, “and these first-time investors are left to figure things out on their own.”

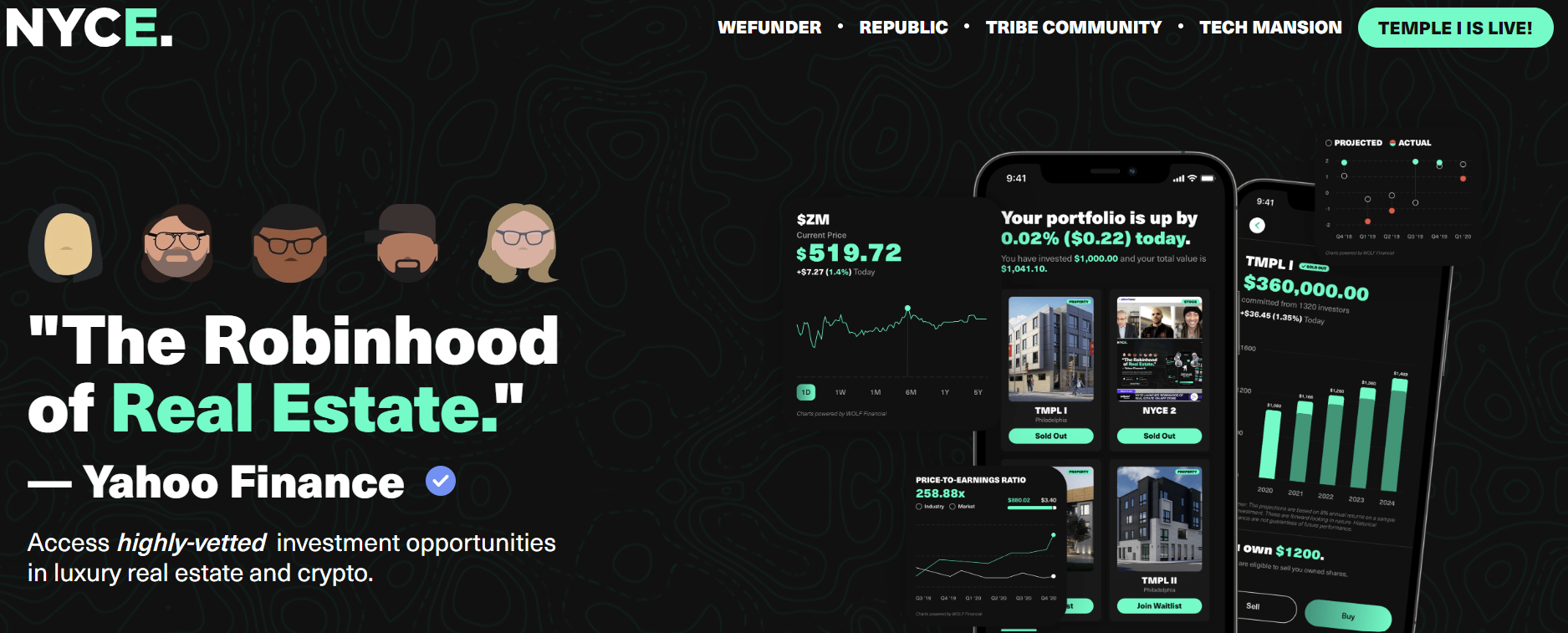

NYCE—a fintech focused on creating wealth for minorities—wants to create 100,000 millionaires through real estate investments and wealth education.

Through its app, investors can own shares in apartment complexes for as little as $100.

Since launching, NYCE has set records for most new first-time BIPOC real estate owners, buying over 1500 apartments in the pandemic and splitting ownership with its investor crowd.

Once investors are in, NYCE automatically enrolls investors in an online wealth academy (TRIBE) that teaches basic wealth principles, responsible investing and how to spot irregular fads like altcoins and meme stocks.

“Becoming a millionaire is a function of time and habit, not luck and one-time scores,” Michael says. “The micro-investments are really just the gateway drug to that wealth mindset.”

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >