Wealth Hacks

Is Work Life Balance A Myth?

You wake up, ugh, another day of work. Is it Friday yet?

You get the kids to school or daycare after a hectic morning and finally punch in at work. Finally, you get to work but have to walk past that one person who’s always smiling and happy, it’s so annoying.

You drone through the day thinking about your weekend plans.

Sure, there are a few faces around the office you like, so the entire day is not wasted. You get to catch up with some pals.

Finally, it’s time to go home. After the commute, it’s basically dinner time when you get home and get the kids to bed.

You sit down and you’re….exhausted. You sit on the couch to rest, and next thing you know it’s getting late and time to go to bed.

Another wasted day…and you think “I wish I had some work-life balance.”

Then you wake up again…

What is Work-Life Balance?

Work-Life balance is the goal of balancing your time between work and other parts of your life including family, social, leisure, and other personal interests…

Guess what. you’re wasting your time…

It’s not because the cause isn’t noble. But then again, people spend their lives trying to find Big Foot, aliens, and the Loch Ness Monster.

If it doesn’t exist, you won’t find it no matter how much you search for it.

A job is like indentured servitude. Unlike indentured servants of the past, you aren’t bound to a specific employer. But, you are bound to employment within the system.

That’s the reason why you’re unhappy and looking for balance

But, you can’t balance that.

Work vs a Job

Work is defined quite simply as an activity involving mental or physical effort done in order to achieve a purpose or result. Or it can be an activity done as a means of earning income.

A job on the other hand is a paid position of regular employment.

Do you see the difference?

Work is an activity, a job involves employment. While they are clearly related, at a minimum we need to see they are different.

If you chase the idea of job-life balance, you’ve accepted that you will always have a job and it is separate entirely from and incompatible with your ‘life’.

Some people can accept their role inside the corporate system. That is the person who is always happy at work. They don’t seek work-life balance because they are content.

Maybe they don’t even recognize what’s controlling their lives, or maybe they don’t care.

Either way, that’s not you. You want something more.

On the other hand, if you pursue some activity that you are passionate about and love that also happens to earn some form of money, you are ‘working’.

Here’s the kicker, If it is a personal interest, passion, or hobby, it’s already part of ‘life’.

…and that’s why chasing work-life balance is like chasing a pot of gold at the end of the rainbow.

You either accept your life as a worker bee, or you are unhappy. There is no way to be a worker bee for a little bit of the time and be a lion on the hunt the rest of the time.

There is simply no way to balance between those two. You need to be one or the other.

You need to accept that you are a worker bee, and be content. OR, you need to be the thing you want to be.

If you are the thing you want to be, there is no need to find a ‘balance’ between being that and being something society needs you to be.

That’s why work-life balance doesn’t exist.

Balance

That all being said, achieving balance is a part of all aspects of life.

Eat too much or eat too little, you end up in the hospital either way.

It’s like all those contradictory food studies – wine is good for you one day and bad for you another day. Or maybe this week it’s potatoes that are good for you or bad for you or… who knows?

That’s because literally everything in life needs to be balanced.

But, that’s just life. Why are we looking at all the various pieces of life that need to be on the scale?

Remember, though, a scale can balance things because it has a fulcrum. And, just as with a scale, your life has a fulcrum as well.

Finding Focus

All scales have a fulcrum and all lives must have a focus.

This is the singular thing that is most influential in your life, which directs or impacts all other decisions in your life.

For some people it’s religion. They always think about what is written about what God wants. Or they pray and look for guidance on various things.

They act either out of love/respect for what they believe God’s wishes are. Sometimes they act out of fear of God’s judgement.

For other people, their lives are balanced around friends, family, their community, or something similar.

They dress a certain way, buy certain types of vehicles, houses, etc because of how their social group will perceive them.

The job and the life of work is chosen because that is what their peers and parents expect them to do.

They want the acceptance of the group, or perhaps fear their judgement.

If you want to change who you are, you need to change the fulcrum and stop focusing on what’s on the plates on either side

That’s how entrepreneurs are different. We create our own businesses and make that our fulcrum.

Your Business as Your Fulcrum

If you love to do something, you’ll naturally want to do it more and other activities just won’t seem as important anymore.

That’s how entrepreneurs can work 12 hours or more, 7 days per week. They burn with passion for it. The business they are building is everything to them.

Of course, no one can work incessantly with no leisure or time with their family.

Maybe they get their spouse and children involved too. So their passion becomes the family passion. Now they spend time together and build their future.

They make new friends and go to dinner or parties with them. These friends are also entrepreneurs who have intense passion as well.

You raise your children and show them how passionate you are and teach them how to find and cultivate their own passions.

As they get older, they learn that life is not about a modern form of cubical slavery, but instead aboutthey pursue those passions and build balanced lives around what makes them burn.

Soon, everything in your life has some piece of your passion in it in some way.

This is balance.

This article originally appeared on IdealREI. Follow them on Facebook, Instagram and Twitter.

In times of economic uncertainty, gold has long been a reliable investment option for those looking to hedge against inflation and volatility.

If you’re looking to invest in the production of gold, as well as gold itself, here are three stocks you can buy inside the NYCE app today.

1. Barrick Gold Corporation (GOLD)

Barrick Gold Corporation is one of the largest gold mining companies in the world with operations in North America, South America, Africa, and Australia.

Performance: Barrick Gold Corporation has experienced steady growth in the past decade, with its stock price increasing by 31% from 2010 to 2020.

Known for: Barrick Gold Corporation is a leader in responsible mining practices, and is committed to environmental sustainability and social responsibility.

NYCE APP CTA:

2. Newmont Corporation (NEM)

Newmont Corporation is one of the world’s leading gold mining companies with operations in North America, South America, Australia, and Africa.

Performance: Newmont Corporation has experienced significant growth in the past decade, with its stock price increasing by 184% from 2010 to 2020.

Known for: Newmont Corporation has a strong track record of responsible mining, and has been recognized as a leader in environmental stewardship and social responsibility.

3. Franco-Nevada Corporation (FNV)

Franco-Nevada Corporation is a royalty and streaming company that provides financing to gold mining companies in exchange for a share of their future production.

Performance: Franco-Nevada Corporation has experienced substantial growth in the past decade, with its stock price increasing by 780% from 2010 to 2020.

Known for: Franco-Nevada Corporation offers investors exposure to the gold industry without the risks associated with mining operations, making it a popular choice among risk-averse investors.

From selling cookies on the streets of New York to sending personalized messages on potatoes, these five entrepreneurs turned their unconventional ideas into multi-million dollar businesse

- “How a High School Dropout Made $10 Million Playing Video Games Online”

This story is about Matthew Haag, also known as Nadeshot.

Nadeshot. 🤨

He dropped out of high school to pursue a career in gaming and became a professional gamer. He has since won multiple championships and has a large following on social media.

- “Meet the Teen Who Turned His Hobby into a $1 Million E-Commerce Business”

This story is about Cory Nieves, also known as Mr. Cory.

Mr. Cory started a cookie business at the age of six, selling cookies on the streets of New York.

He eventually turned his hobby into a successful e-commerce business, selling cookies online and in stores.

He has been featured on various media outlets and has even baked cookies for Oprah Winfrey.

- “The Surprising Story of the Stay-at-Home Mom Who Made $100K in One Year Blogging About Knitting”

This story is about Sarah Corey, who started a knitting blog called “My Simple Knitting” while staying at home to raise her children.

Her blog became popular and she eventually started selling knitting patterns and products.

She made over $100K in one year from her blog and has since turned her passion for knitting into a successful business.

- “How One Man’s Love for Potatoes Turned into a $5 Million Online Business”

This story is about Alex Craig, who started a website called Potato Parcel where he would send personalized messages on potatoes.

His business gained popularity and he has since expanded into other products, such as potato socks and potato candles.

He has been featured on various media outlets and his business has grown to make millions of dollars in revenue.

- “Pet Rock Creator Gary Dahl Turned a Silly Idea into a Million-Dollar Business”

This story is about Gary Dahl, who famously created and marketed Pet Rocks in the 1970s.

Despite being a seemingly ridiculous idea, the Pet Rock became a massive success, with Dahl selling millions of Pet Rocks and becoming a millionaire in the process.

READ: How This 9-5’er Made Millions Selling Free Rocks In His Spare Time

wealthlab is a platform for hustlers, doers, entrepreneurs and investors to do epic s&%. Our mission is to create 100M new investors worldwide. Join our academy here.*

Don’t miss:

- ‘I work just 2 hours a day’: A 24-year-old who makes $8,000 a month in passive income shares her best business advice

- This 38-year-old makes $160,000 per month in passive income—after losing his job: ‘I work only 5 hours a week now’

- This 33-year-old mom makes $760,000 a year in passive income—and lives on a sailboat: ‘I work just 10 hours a week’

Sign up now: Learn how to retire with $1M with our wealth academy.

Yes, you read that right.

If there’s anything the pandemic taught us, it’s that the paradigm of “office” and “workspace” has been shaken to its CORE.

Universities are teaching via Zoom, court dates are done virtually, FULLY REMOTE businesses are valued at $1B+, and legitimate Inc. 5000 startups are run from…wherever. 📲

This is my office for the day…

I am actually running our business from the beach, typing this from here.

It’s 4:28 pm CET, which means it’s 10:28 am EST and I am CRUSHING my to-do list.

(And the team will continue to crush it while I’m asleep. That’s the 🗝)

So how did we get here?

We launched NYCE and our mission to create 100,000 millionaires in March, 2020…just as the global COVID-19 lockdown happened. 😳

As a result, we shut down our main office and set EVERYTHING up to run remotely…

SMOOTHLY! And a system that allows us to outperform competition by 200%. (You can build this system, too. More on this in a second.)

Here’s what we were able to do since then:

- Gained 6M+ followers across all platforms 📈

- Add 1500+ new apartments to the portfolio 🤑

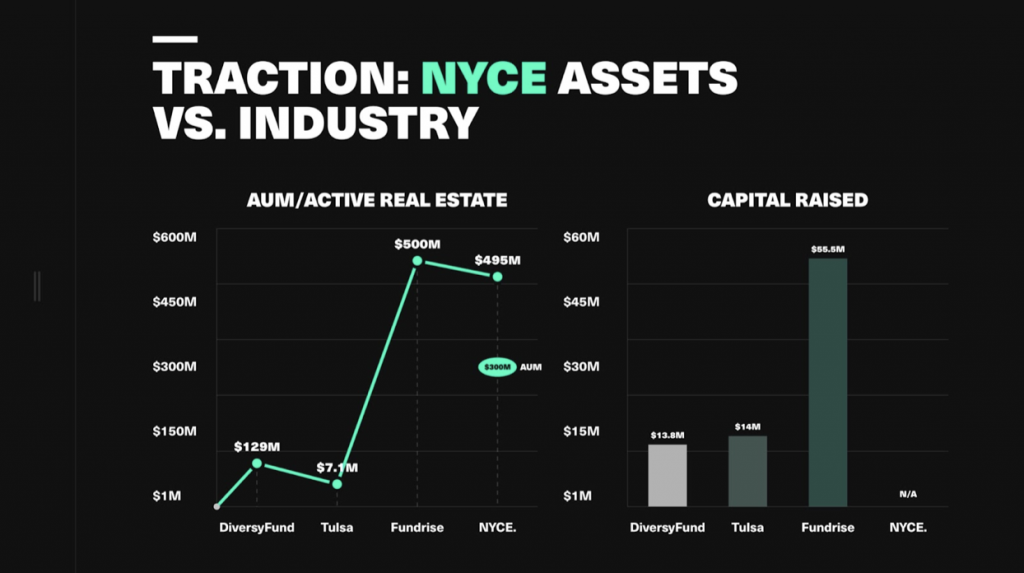

- Grow to $300M in real estate 🚀

- 105% investor returns 🎉

- 700K+ community members 🤝

And here’s the best part…

Having team members in all the main time zones gives us a 24-hour work cycle vs. 9-5/eight-hour on-the-clock performance.

This means we get 3x the productivity of a similar company. 🔥

Let me repeat that…3x PRODUCTIVITY vs. our competitors.

Meanwhile our project management software grants us 24-hour TEAM-WIDE connectivity that tracks all tasks and lets us know if productivity dips even a little bit.

There is ALWAYS someone senior awake. It could be Martin in Barcelona…Nat in New York…Vineet & Arif in New Delhi.

All the while giving YOU GUYS wealth hacks and daily content. 🔥

OK, so how can you do it?!

Well, the first step is to have an actual side hustle you’re launching. Not just an idea, a validated business.

MAJOR KEY: Do NOT spend money until you’ve made your FIRST DOLLAR! 🗝🗝🗝🗝

(You can catch a replay Business Launch masterclass here and see TRIBE member Nessa launched her business on the spot and got her first $45K client shortly after.)

One of the easiest ways to start is with Airbnb—you can start that in 10 minutes. Literally. (Here’s a guide if you need it.)

Once you have your business, you build a virtual infrastructure (you really just need two softwares, which are FREE), manage the team accordingly and run the business from there.

I’m gonna put together a step-by-step video breakdown this weekend inside the new TRIBE U on the FIVE key things you need to do this for YOURSELF. 💵 💎

From what software to use, how to build a team, how to keep.

In the meantime, drop a comment if you’re ready to build some wealth and any questions if you want more…

Let’s get to work. 🙌

PS: If you can’t be bothered with video and just wanna get to work, we’re hosting a TRIBE U workshop that will help you get this process started on the spot. It’s $479 $49. 🔥

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login