Wealth Hacks

How To Preserve Family Wealth By Planning For Succession

In the UK alone, an estimated £5.5 trillion is due to be passed between generations over the next 30 years – according to Kings Court Trust – yet according to the Attitudes Survey 2019, only half of Ultra High Net Worth Individuals have a robust succession plan in place.

Most inheritance handovers will be seamless. However, lack of a succession plan is a concern because it takes time to devise a holistic strategy to transfer decision-making responsibilities to the next generation. Not surprisingly, there are numerous barriers to the process: timing, lack of clear objectives and in some cases the decision maker or head of the family might not be ready to hand over authority.

Alongside all this, changing family structures and a wide span of generations present challenges of their own. For example, children in different branches of the family might be treated differently, as might stepchildren and grandchildren, particularly concerning property or fine art.

Passing on wealth is a major concern for wealthy families and while there is no way of rubber stamping the transfer process, there are three approaches that one can take to prepare for successful transition.

Promoting a vision

Apart from wanting to provide a comfortable level of wealth to future generations, it is important to start by identifying clear objectives: defining how future generations should benefit from an inheritance; identifying what that might mean, to whom and in what proportions.

Some families want to maintain consistency in their philanthropic ventures, while others are more focused on creating a lasting legacy. Is there a philanthropic purpose for your wealth and if so, does it align with your family’s values? For instance, there are hundreds of foundations dedicated to different causes; from well-known ones such as the Wellcome Trust to the smaller such as the Peter Harrison Foundation. Each one has its own mission.

Sometimes the interests and focus of the head of the family do not align with the children or grandchildren. For example, baby boomers might be comfortable investing in manufacturing, but Gen X and Gen Y might prefer an emphasis on sustainable investing or in technology venture capital. There will even be wide disparities in risk tolerance amongst the beneficiaries. And then there are myriad human factors; everyone will have different personal views, experiences and needs.

Preparing the legacy

At the same time, it is important to create the right governance structures and identify the corporate trustees and lawyers that will assist you in achieving the smooth transition of assets.

Taking an integrated approach with this is one of the keys to successful transfer and management of wealth. For example, what type of structures should be established; trusts, private trust companies, foundations or even groups of companies? Co-ordinating with the relevant experts depending on the assets held and structures required is essential too.

Clients with family located internationally will need to understand the implications to the wealth transfer of offshore and regional tax regimes, for example. Even US and UK FATCA and the automatic exchange of information need to be taken into account.

It’s all about the people

Wealth transfer is of course about preservation of assets, but it is also about people. The succession structure needs to fit the individuals within the family. Some members of a family might have little understanding about finance so it might be necessary to educate them or even negotiate with them for the transition ahead. More competent individuals might want a more flexible structure in order to apply their knowledge.

It is therefore vital that the succession planning process, which can take up to a decade, includes open dialogue with key beneficiaries right from the start. A survey conducted by Moore Stephens found that nearly a quarter of respondents highlighted the difficulties when trying to reach agreements in the decision-making process.

It is quite common for people to avoid discussions about money and lack of communication can seriously hinder the process; beneficiaries need to know more than just the names of trustees or advisers.

At JAR Capital, I advise clients to include their beneficiaries gradually. To begin with it might just be an exercise in sharing information, but over time the next generation becomes more interested and seeks to take on more responsibility. This could include taking an active role in investments and governance or spearheading the family foundation.

There is no doubt that issue of intergenerational wealth transfer is a thorny one. Nevertheless, we believe that those families that take action in advance to preserve their wealth for future generations will ensure an orderly and harmonious succession of assets.

This article originally appeared on ValueWalk. Follow ValueWalk on Twitter, Instagram and Facebook.

In times of economic uncertainty, gold has long been a reliable investment option for those looking to hedge against inflation and volatility.

If you’re looking to invest in the production of gold, as well as gold itself, here are three stocks you can buy inside the NYCE app today.

1. Barrick Gold Corporation (GOLD)

Barrick Gold Corporation is one of the largest gold mining companies in the world with operations in North America, South America, Africa, and Australia.

Performance: Barrick Gold Corporation has experienced steady growth in the past decade, with its stock price increasing by 31% from 2010 to 2020.

Known for: Barrick Gold Corporation is a leader in responsible mining practices, and is committed to environmental sustainability and social responsibility.

NYCE APP CTA:

2. Newmont Corporation (NEM)

Newmont Corporation is one of the world’s leading gold mining companies with operations in North America, South America, Australia, and Africa.

Performance: Newmont Corporation has experienced significant growth in the past decade, with its stock price increasing by 184% from 2010 to 2020.

Known for: Newmont Corporation has a strong track record of responsible mining, and has been recognized as a leader in environmental stewardship and social responsibility.

3. Franco-Nevada Corporation (FNV)

Franco-Nevada Corporation is a royalty and streaming company that provides financing to gold mining companies in exchange for a share of their future production.

Performance: Franco-Nevada Corporation has experienced substantial growth in the past decade, with its stock price increasing by 780% from 2010 to 2020.

Known for: Franco-Nevada Corporation offers investors exposure to the gold industry without the risks associated with mining operations, making it a popular choice among risk-averse investors.

From selling cookies on the streets of New York to sending personalized messages on potatoes, these five entrepreneurs turned their unconventional ideas into multi-million dollar businesse

- “How a High School Dropout Made $10 Million Playing Video Games Online”

This story is about Matthew Haag, also known as Nadeshot.

Nadeshot. 🤨

He dropped out of high school to pursue a career in gaming and became a professional gamer. He has since won multiple championships and has a large following on social media.

- “Meet the Teen Who Turned His Hobby into a $1 Million E-Commerce Business”

This story is about Cory Nieves, also known as Mr. Cory.

Mr. Cory started a cookie business at the age of six, selling cookies on the streets of New York.

He eventually turned his hobby into a successful e-commerce business, selling cookies online and in stores.

He has been featured on various media outlets and has even baked cookies for Oprah Winfrey.

- “The Surprising Story of the Stay-at-Home Mom Who Made $100K in One Year Blogging About Knitting”

This story is about Sarah Corey, who started a knitting blog called “My Simple Knitting” while staying at home to raise her children.

Her blog became popular and she eventually started selling knitting patterns and products.

She made over $100K in one year from her blog and has since turned her passion for knitting into a successful business.

- “How One Man’s Love for Potatoes Turned into a $5 Million Online Business”

This story is about Alex Craig, who started a website called Potato Parcel where he would send personalized messages on potatoes.

His business gained popularity and he has since expanded into other products, such as potato socks and potato candles.

He has been featured on various media outlets and his business has grown to make millions of dollars in revenue.

- “Pet Rock Creator Gary Dahl Turned a Silly Idea into a Million-Dollar Business”

This story is about Gary Dahl, who famously created and marketed Pet Rocks in the 1970s.

Despite being a seemingly ridiculous idea, the Pet Rock became a massive success, with Dahl selling millions of Pet Rocks and becoming a millionaire in the process.

READ: How This 9-5’er Made Millions Selling Free Rocks In His Spare Time

wealthlab is a platform for hustlers, doers, entrepreneurs and investors to do epic s&%. Our mission is to create 100M new investors worldwide. Join our academy here.*

Don’t miss:

- ‘I work just 2 hours a day’: A 24-year-old who makes $8,000 a month in passive income shares her best business advice

- This 38-year-old makes $160,000 per month in passive income—after losing his job: ‘I work only 5 hours a week now’

- This 33-year-old mom makes $760,000 a year in passive income—and lives on a sailboat: ‘I work just 10 hours a week’

Sign up now: Learn how to retire with $1M with our wealth academy.

Yes, you read that right.

If there’s anything the pandemic taught us, it’s that the paradigm of “office” and “workspace” has been shaken to its CORE.

Universities are teaching via Zoom, court dates are done virtually, FULLY REMOTE businesses are valued at $1B+, and legitimate Inc. 5000 startups are run from…wherever. 📲

This is my office for the day…

I am actually running our business from the beach, typing this from here.

It’s 4:28 pm CET, which means it’s 10:28 am EST and I am CRUSHING my to-do list.

(And the team will continue to crush it while I’m asleep. That’s the 🗝)

So how did we get here?

We launched NYCE and our mission to create 100,000 millionaires in March, 2020…just as the global COVID-19 lockdown happened. 😳

As a result, we shut down our main office and set EVERYTHING up to run remotely…

SMOOTHLY! And a system that allows us to outperform competition by 200%. (You can build this system, too. More on this in a second.)

Here’s what we were able to do since then:

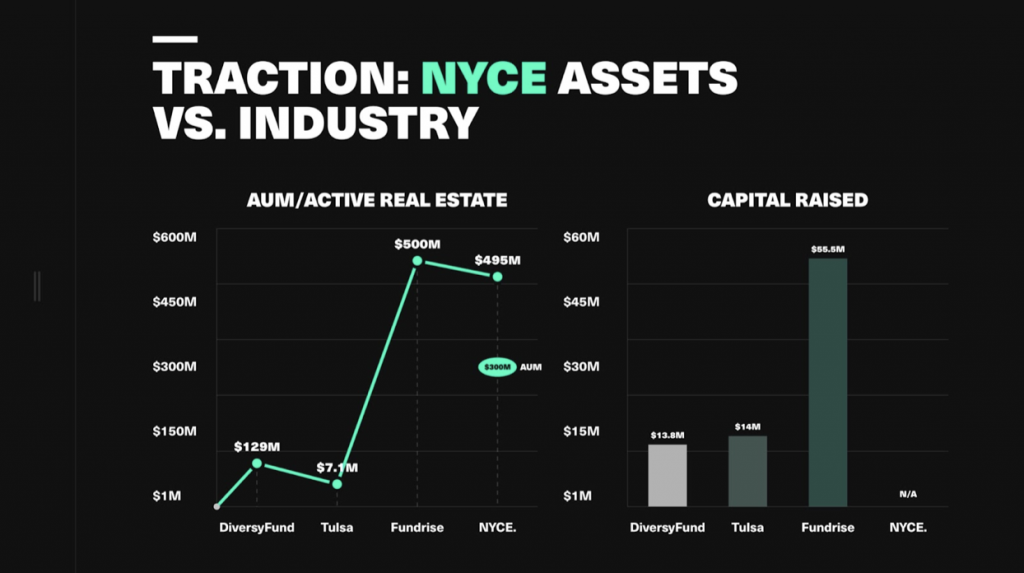

- Gained 6M+ followers across all platforms 📈

- Add 1500+ new apartments to the portfolio 🤑

- Grow to $300M in real estate 🚀

- 105% investor returns 🎉

- 700K+ community members 🤝

And here’s the best part…

Having team members in all the main time zones gives us a 24-hour work cycle vs. 9-5/eight-hour on-the-clock performance.

This means we get 3x the productivity of a similar company. 🔥

Let me repeat that…3x PRODUCTIVITY vs. our competitors.

Meanwhile our project management software grants us 24-hour TEAM-WIDE connectivity that tracks all tasks and lets us know if productivity dips even a little bit.

There is ALWAYS someone senior awake. It could be Martin in Barcelona…Nat in New York…Vineet & Arif in New Delhi.

All the while giving YOU GUYS wealth hacks and daily content. 🔥

OK, so how can you do it?!

Well, the first step is to have an actual side hustle you’re launching. Not just an idea, a validated business.

MAJOR KEY: Do NOT spend money until you’ve made your FIRST DOLLAR! 🗝🗝🗝🗝

(You can catch a replay Business Launch masterclass here and see TRIBE member Nessa launched her business on the spot and got her first $45K client shortly after.)

One of the easiest ways to start is with Airbnb—you can start that in 10 minutes. Literally. (Here’s a guide if you need it.)

Once you have your business, you build a virtual infrastructure (you really just need two softwares, which are FREE), manage the team accordingly and run the business from there.

I’m gonna put together a step-by-step video breakdown this weekend inside the new TRIBE U on the FIVE key things you need to do this for YOURSELF. 💵 💎

From what software to use, how to build a team, how to keep.

In the meantime, drop a comment if you’re ready to build some wealth and any questions if you want more…

Let’s get to work. 🙌

PS: If you can’t be bothered with video and just wanna get to work, we’re hosting a TRIBE U workshop that will help you get this process started on the spot. It’s $479 $49. 🔥

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >