Business

(WTF?!) Is The MBA Dead?

Well, well, well, what do we have here.

So according to a (totally non-biased) press release from the Graduate Management Admission Council (GMAC) earlier this year, MBA grads are making more money than ever.

(Just for clarity, the GMAC is a “global association of leading graduate business schools.”)

Apparently, US employers plan to offer new MBA hires a starting salary of $115,000, the highest ever recorded in the US when adjusted for inflation.

Key words: PLAN. TO.

In spite of these lofty, non-scientific projections, the number of MBA applications—as a whole—is on the downslide. Here’s a chart from the otherwise very optimistic GMAC.

(Yes, the entire WealthLAB crew is MBAs, too. Jury’s still out whether that makes us marks or smart. 🙄)

And according to Forbes, this makes it the best time ever to pursue an Ivy League MBA.

So what does this all mean? Let’s unpack it for a second.

Top 10 programs are letting everyone in…

According to the various reports, some programs across the country have seen double-digit drops, with the top 10 business schools seeing serious declines.

At the highly selective Yale University, the acceptance rate jumped by nearly 44%. Dartmouth College’s Tuck School of Business, another Top 10 program, admitted more than one in three of its applicants, a 48% increase in a single year.

Meanwhile its applications dropped by 22.5%.

“The joke among deans is that ‘flat is the new up,'” Andrew Ainslie, the dean of the University of Rochester’s Simon School of Business. “If we can just hold our numbers, that is an incredible achievement.”

Other Ivy League schools have dropped also, with Harvard measuring a fall of 4.5%. Meanwhile, big names like Stanford saw a bit more at 4.6% and UC-Berkeley Haas at a shaking 7.5%.

And outside the Top 10?

When these numbers are narrowed down to individual schools, like University of Michigan Ross School of Business, the picture gets worse. This university saw the biggest reduction, noting an 8.5% decline with just over 3,000 candidates applying.

There are only a few reported exceptions to this overall decline, but the biggest business schools in the nation agree that there is a serious reduction in MBA interest.

Ainslie says up to 20% of the top 100 MBA programs in the country are likely to close in the next few years.

But why?

Uncertainty over work visas for international students, the strong US economy with decreasing job loss, and the rising costs of degrees are all noted as potential causes.

The positive side to the story, as Ainslie pointed out, is that it’s going to spark new development in the design of existing MBA programs. One particular program has been built around entrepreneurship.

In addition, the prestigious post-MBA job paths—think investment banking and management consulting—have been replaced by jobs in the tech world and Silicon Valley.

Is entrepreneurship the new MBA?

“Tech has displaced consulting and finance as the preferred career path for top-tier college students,” says David Minnick, founder and CEO of Camino Data, and former president of beverage company, Purity Organic.

“When I started Princeton in 2003, it was still a big deal to get a MBA or JD/MBA after college,” he tells Forbes. “That was the thing to do.

“Four years later, when I graduated, we wanted to be more entrepreneurial. We saw people who had started successful tech businesses. We saw there were low barriers to entry, and that it was okay to fail.”

Image: Dunk The sum total of all human knowledge via @James_Kpatrick/ Flickr

Student debt vs. MVP?

There’s also the whole cost thing. Business school can run you $200,000, making it a cringe option for 20-somethings already riddled with debt. For founders, this is money better spent building an MVP.

(No, not Most Valuable Player. Minimum Viable Product.)

Not to mention the experience it brings.

“When I interviewed people with an MBA, or experience at a big beverage company like Coke or Pepsi,” says Minnick, :I was concerned that their personality type wouldn’t be the right fit for a young and growing company like ours.”

In his view, hustle, skills and culture fit are far better predictors of performance than a degree.

Ivy League MBA fire sale…🗑

Apparently this all means that IF you are one who’s always dreamed of an MBA from a prestigious school, there’s no better time than now.

“With an unprecedented decline in MBA application volume at many business schools – including iconic, top-tier programs – there’s definitely a ‘perfect storm’ happening for prospective applicants,” Alex Min, CEO of The MBA Exchange, a top admissions consulting firm, says.

“Deans and admissions committees are feeling strong pressure to fill available seats with qualified candidates, even if some of these individuals might not have been admitted in previous years when application volume was growing.”

Yes, you read that right.

If there’s anything the pandemic taught us, it’s that the paradigm of “office” and “workspace” has been shaken to its CORE.

Universities are teaching via Zoom, court dates are done virtually, FULLY REMOTE businesses are valued at $1B+, and legitimate Inc. 5000 startups are run from…wherever. 📲

This is my office for the day…

I am actually running our business from the beach, typing this from here.

It’s 4:28 pm CET, which means it’s 10:28 am EST and I am CRUSHING my to-do list.

(And the team will continue to crush it while I’m asleep. That’s the 🗝)

So how did we get here?

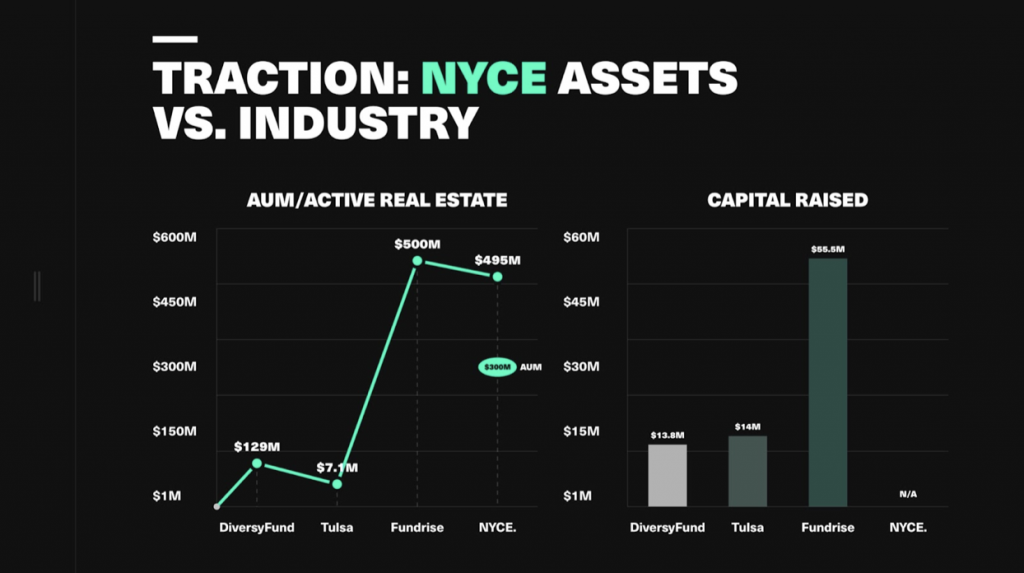

We launched NYCE and our mission to create 100,000 millionaires in March, 2020…just as the global COVID-19 lockdown happened. 😳

As a result, we shut down our main office and set EVERYTHING up to run remotely…

SMOOTHLY! And a system that allows us to outperform competition by 200%. (You can build this system, too. More on this in a second.)

Here’s what we were able to do since then:

- Gained 6M+ followers across all platforms 📈

- Add 1500+ new apartments to the portfolio 🤑

- Grow to $300M in real estate 🚀

- 105% investor returns 🎉

- 700K+ community members 🤝

And here’s the best part…

Having team members in all the main time zones gives us a 24-hour work cycle vs. 9-5/eight-hour on-the-clock performance.

This means we get 3x the productivity of a similar company. 🔥

Let me repeat that…3x PRODUCTIVITY vs. our competitors.

Meanwhile our project management software grants us 24-hour TEAM-WIDE connectivity that tracks all tasks and lets us know if productivity dips even a little bit.

There is ALWAYS someone senior awake. It could be Martin in Barcelona…Nat in New York…Vineet & Arif in New Delhi.

All the while giving YOU GUYS wealth hacks and daily content. 🔥

OK, so how can you do it?!

Well, the first step is to have an actual side hustle you’re launching. Not just an idea, a validated business.

MAJOR KEY: Do NOT spend money until you’ve made your FIRST DOLLAR! 🗝🗝🗝🗝

(You can catch a replay Business Launch masterclass here and see TRIBE member Nessa launched her business on the spot and got her first $45K client shortly after.)

One of the easiest ways to start is with Airbnb—you can start that in 10 minutes. Literally. (Here’s a guide if you need it.)

Once you have your business, you build a virtual infrastructure (you really just need two softwares, which are FREE), manage the team accordingly and run the business from there.

I’m gonna put together a step-by-step video breakdown this weekend inside the new TRIBE U on the FIVE key things you need to do this for YOURSELF. 💵 💎

From what software to use, how to build a team, how to keep.

In the meantime, drop a comment if you’re ready to build some wealth and any questions if you want more…

Let’s get to work. 🙌

PS: If you can’t be bothered with video and just wanna get to work, we’re hosting a TRIBE U workshop that will help you get this process started on the spot. It’s $479 $49. 🔥

Investor and popular Instagram influencer Philip Michael says new fintechs need to take greater responsibility for their younger traders.

“Promoting financial literacy is a must, but encouraging risky gambling is reckless,” Philip Michael, NYCE CEO, says.

In 2020, a 20-year-old Robinhood trader killed himself after engaging in risky options trading and seeing his balance $730,000 in the red, leading to a wrongful death lawsuit against the investment app.

“The main apps onboard as many new users as humanly possible, but there’s really no educational process,” Michael says, “and these first-time investors are left to figure things out on their own.”

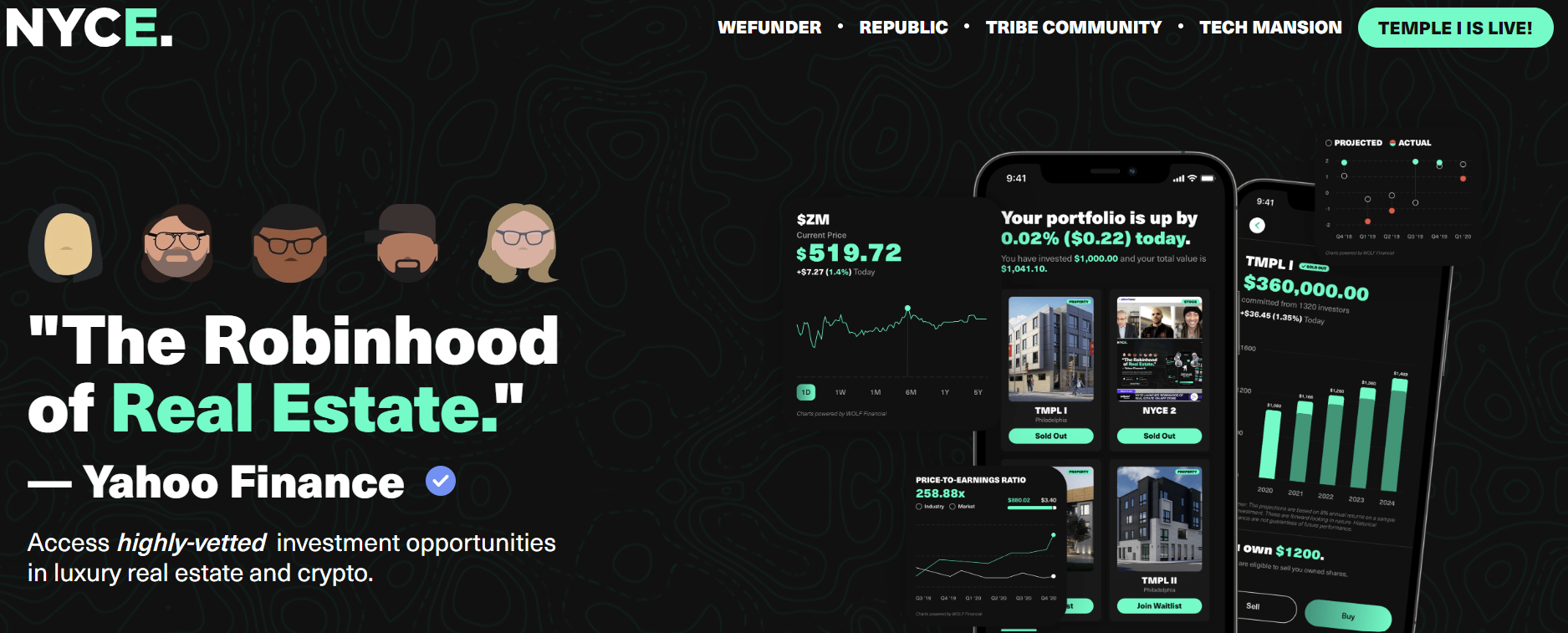

NYCE—a fintech focused on creating wealth for minorities—wants to create 100,000 millionaires through real estate investments and wealth education.

Through its app, investors can own shares in apartment complexes for as little as $100.

Since launching, NYCE has set records for most new first-time BIPOC real estate owners, buying over 1500 apartments in the pandemic and splitting ownership with its investor crowd.

Once investors are in, NYCE automatically enrolls investors in an online wealth academy (TRIBE) that teaches basic wealth principles, responsible investing and how to spot irregular fads like altcoins and meme stocks.

“Becoming a millionaire is a function of time and habit, not luck and one-time scores,” Michael says. “The micro-investments are really just the gateway drug to that wealth mindset.”

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >