Real Estate Investing

Is The 1% Rule Garbage?

There’s a lot of “rules of thumb” floating around out there related to real estate. The one I hate the most is the 1% rule.

It’s wrong. It doesn’t work. Period.

Let me explain…

The 1% Rule Explained

Let me take a step back and explain the 1% rule first.

In a nutshell, it says that the monthly rent for your rental property should be at least 1% of the property value. If you can meet this goal then you can make some good money in real estate.

So, if you find a property that rents for $1,000/month and you can negotiate a price of $100,000 then you’re in good shape.

…at least according to the people pushing the 1% rule.

Breaking Down the 1% Rule

Let’s say that that you find a property that is $100,000 and rents for $1,000.

We know around 5-10% goes straight to vacancy. So, that leaves you $900.

And 50% of that goes to expenses. Leaving you with $450.

And a 30 year mortgage on an $80,000 loan (I assume 20% was put down) is around $429.

So, that leaves you around $20 – $70 (depending on vacancy) each month.

…not very sexy is it?

The Break Even Ratio

Traditionally, the 1% rule was considered the break even rule. Where you would most likely cover your debt when rents are 1% of your purchase price.

So, what happened?

I don’t know for a fact, but I think a couple of things happened.

Turnkey Real Estate Companies

First, I think that turnkey companies started pushing it as a solution. A turnkey company finds a distressed property, rehabs it, puts a tenant in there and sells it to you for at or above market price.

There is definitely some value to what turnkey companies do, but often they based their prices on the 1% rule and not necessarily on market value. That allows them to get higher prices in generally low cost markets.

They justify it with free education. They teach you that if you can get 1% of the value as rent, then the deal is great and you can make a ton of money…

To people on the west coast or other high-cost areas, this seems awesome because the ratios there are closer to 0.5%. So, relatively speaking, they are “great deals” even though they are overpaying.

Inexperienced Gurus

There are a ton of new gurus out there pushing all kinds of different ideas. Some are good and some are not, but the 1% rule keeps popping up, especially with online education.

Often, these are run by people who own a few properties and have done really well since the recession. It makes sense if you think about it. If you bought at 1% back then and rents and prices have almost doubled, then you are way above 1% based on what you purchased it for.

But, that is buying based on speculation that the market will improve, not based on the fundamentals of the deal.

Another common guru you see out there now is someone who’s only been investing for a few years. Even if they are doing great but they haven’t really been around long enough to see and understand the nuances.

They don’t realize that the 1% rule works when there are massive rent growth and appreciation but could never work in a sideways or downward trending market.

What About Using it As a Filter?

People will suggest using the 1% rule as a filter to go through hundreds of deals quickly. Here’s how they suggest you do it:

list all the prices, list all the rents, then calculate the ratios. Anything under 1% toss out and anything over 1% keep and look at deeper. So, a spreadsheet might look like this.

Based on this, you should consider buying the first, third, and fifth property on the list because the ratios are all above 1%.

But, this is missing a HUGE amount of detail. What is most important is not what it’s receiving for rent today, but what it could be receiving after you own it. So, you should based your numbers on potential rent not current rents.

Based on the new spreadsheet, the best potential deals are the 4th and 6th. While others may have potential as well based on the 1% rule, you see some really good ratios on deals you would have previously discarded.

That’s why the 1% rule is kind of silly. It leads you to discard potentially great deals in favor of more marginal deals.

Focus on The Numbers

The rent to price ratio is an important ratio to consider before purchasing anything. Just remember, it is a rule of thumb. Also, remember what it truly means:

The 1% rule is the break even rule not a rule to earn you money.

Rules of thumb are designed as a reality check. Things like the 50% rule to expenses or the 1% rule are there to act as a guide. If you are running the numbers and you’re rent is 1.5% while everyone else is at .75%, then you should think twice.

Or, perhaps your expenses are at 25% and everyone else is running at 50%. Then you should double check.

They are not and should never be used to make a buying decision.

That’s why I give away simple calculators like this one, to point you in the right direction.

This article originally appeared on IdealREI. Follow them on Facebook, Instagram and Twitter.

By Sheryl Chapman

As we all know, the economy can be unpredictable at times. Recession is a common phenomenon that can affect the investments in your portfolio.

But don’t worry, there are some sectors that are likely to perform well—even during a recession. Here are five recession-proof investments that you can consider adding to your portfolio.

(Editor’s note***********:************ If you wanna learn how to start investing for retirement, check out the free lessons inside the academy! 📺)*

1. Consumer staples

Consumer staples are products that are essential to our daily lives, such as food, household goods, and personal care items.

These products are in constant demand, regardless of the economic climate. Companies that produce these items, such as Procter & Gamble and Coca-Cola, are considered recession-proof investments.

These companies have a stable revenue stream that can weather economic downturns.

2. Utilities

Utilities are another recession-resistant investment. People need electricity, gas, and water, regardless of the state of the economy.

Utility companies, such as Duke Energy and American Electric Power, have a steady stream of revenue and provide investors with a reliable source of income.

3. Healthcare

The healthcare industry is recession-proof because it provides essential services that people cannot do without. Companies that provide healthcare services or products, such as Johnson & Johnson and UnitedHealth Group, are likely to remain profitable during a recession.

4. Gold

Gold is a safe-haven investment that many investors turn to during times of economic uncertainty. Gold prices tend to rise during recessions because it is seen as a store of value. Investors can buy physical gold, gold ETFs, or invest in gold mining stocks.

GUIDE: 3 Ways To Invest In Gold In 3 Minutes Or Less 🔑📲

5. Treasury bonds

Treasury bonds are considered to be one of the safest investments during a recession.

These bonds are issued by the US government and are backed by the full faith and credit of the government. Treasury bonds provide a fixed income and are considered to be a low-risk investment.

In conclusion, these five investments are considered to be recession-proof because they provide essential products or services that people cannot do without.

Adding these investments to your portfolio can provide stability during times of economic uncertainty.

Airbnb has revolutionized the travel industry by providing an affordable and unique way for travelers to experience different destinations.

With over 7 million listings worldwide, it’s safe to say that Airbnb has become one of the most popular ways for travelers to find lodging.

However, as a host, one of the most challenging decisions you’ll face is determining the right price for your listing.

Pricing your Airbnb listing correctly is critical to your success as a host, as it can make or break your profitability.

Here are some tips to help you price your Airbnb listing for maximum profit:

Know Your Market

Before you set your price, it’s essential to research the market in your area. Look at other listings in your neighborhood, paying attention to the size of the property, amenities, and location. Check the availability of your competitors and the average price they charge. This information will help you determine your pricing strategy and ensure that your listing is competitive.

Consider Seasonal Demand

Seasonal demand plays a significant role in the pricing of your Airbnb listing. During peak seasons, such as holidays, festivals, and major events, you can charge higher rates. Conversely, during low seasons, you’ll need to lower your prices to attract guests. Keep track of events happening in your area and adjust your prices accordingly.

Offer Discounts

Offering discounts is an effective way to attract guests and increase your occupancy rate. Consider offering discounts for extended stays, early bookings, or last-minute reservations. You can also offer discounts to guests who leave a positive review or refer new guests to your listing.

Calculate Your Costs

To ensure that your pricing strategy is profitable, you need to calculate your costs. Take into account expenses such as cleaning fees, utilities, maintenance, and taxes. Factor in your time and effort as well. Your goal is to set a price that will cover all your costs while still allowing you to make a profit.

Be Flexible

Finally, be flexible with your pricing strategy. Test different prices and see how they affect your occupancy rate and profitability. Monitor your competition regularly and adjust your prices accordingly. Remember that the market is constantly changing, and your pricing strategy needs to adapt to stay competitive.

In conclusion, pricing your Airbnb listing for maximum profit is a crucial aspect of your success as a host. By researching your market, considering seasonal demand, offering discounts, calculating your costs, and being flexible, you can set the right price for your listing and maximize your profitability.

Happy hosting!

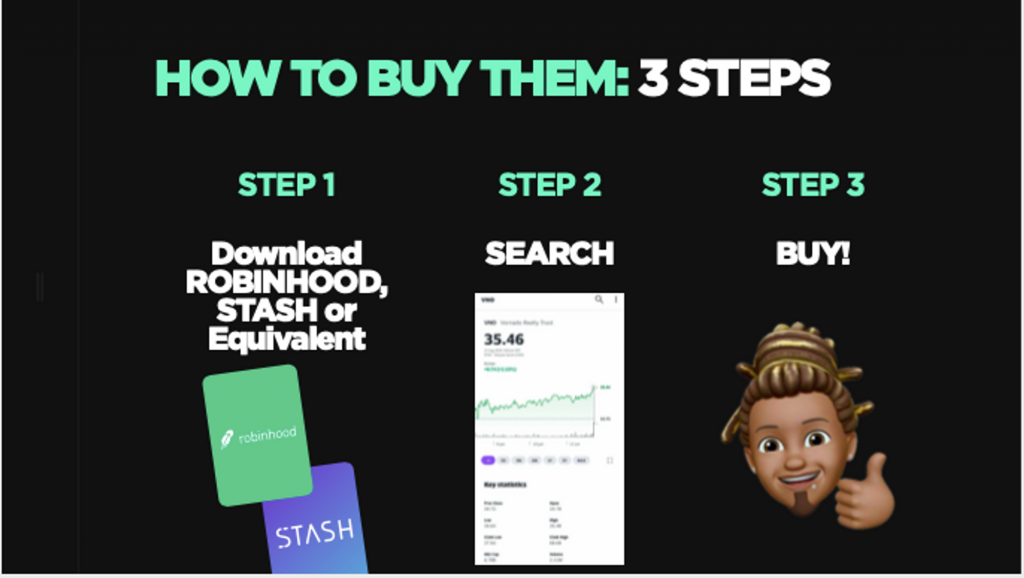

5 REITs that own iconic buildings you can buy today

Real Estate Investment Trusts (REITs) are companies that own and operate income-generating real estate properties.

Investing in REITs has become an increasingly popular way to own a piece of the real estate market without having to buy individual properties.

And you can buy them in the next 5 minutes on the NYCE app…with $5 or less.

Here are five REITs that own iconic buildings across the United States that you can invest in today:

- Empire State Realty Trust, Inc. (ESRT) – ESRT owns the famous Empire State Building in New York City, as well as several other properties in the city.

- Vornado Realty Trust (VNO) – VNO owns the iconic 555 California Street building in San Francisco, which was once the tallest building on the West Coast.

- Boston Properties, Inc. (BXP) – BXP owns several iconic buildings in the United States, including the John Hancock Tower in Boston and the Salesforce Tower in San Francisco.

- SL Green Realty Corp. (SLG) – SLG owns several iconic properties in New York City, including One Vanderbilt, which is currently the fourth-tallest building in the city.

- Macerich Company (MAC) – MAC owns several high-end shopping centers across the United States, including the iconic Santa Monica Place in California.

************************************************************************************************LEARN: How to own real estate with $1000 or less.

Investing in REITs can provide diversification and potentially higher returns than investing in individual properties. However, as with any investment, it is important to do your research and understand the risks involved.

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >