Business

How To Prevent Cash Flow From Ruining Your Business

There are many potential threats to your business, which you’ll have to manage on an ongoing basis. Competition could move in to threaten your territory. Defective products could cause you to lose consumer confidence. Your employees could leave or stop caring about the business. But one of the most dangerous threats is cash flow-the volume of cash coming into and going out of the business at any given time. If your business reaches negative cash flow and you have no way to compensate for it or recover, your business could go under.

So why does cash flow have the power to kill so many businesses, and what can you do to protect yours?

The Power of Cash Flow

Let’s start by evaluating why cash flow is so important to the life and sustainability of a given business. Cash represents your buying power, and your buying power is necessary for most aspects of your business. For example, you’ll need cash on hand to maintain your office and equipment, pay your vendors, and keep paying your employees. If you’re defaulting on your loans and your employees aren’t getting a paycheck, it won’t be long before your business is forced to close its doors.

Cash flow is also a point of vulnerability because it’s affected by multiple variables. Multiple elements of business management could impact the state of your cash flow, including:

- How many paying customers you have. If you’re dealing with a customer shortage, you won’t have enough incoming revenue to cover your expenses, forcing you to tap your lines of credit (until they, too, inevitably dry up).

- How you invoice your customers. Using a reliable invoice template will help you invoice your customers consistently. If you forget to send invoices, or if you don’t follow up on invoices you’ve sent that haven’t been paid, eventually, you’ll end up with a cash flow shortage.

- How you manage expenses. Buying too much at once or allowing your expenses to accumulate endlessly can put a huge burden on your cash flow management.

- How you pay your bills. Even the timing of your bill payments can have an impact on your cash flow, if you needlessly drain your cash to pay a bill prematurely.

All it takes is one major disruption in one of these areas to create a cash flow problem, and if that problem is allowed to grow worse, that could be it for your business.

Improving Cash Flow in Your Business

So what steps can you take to improve your cash flow?

- Appoint a cash flow authority. First, it’s a good idea to put someone in charge of cash flow management. This designated authority, usually someone in your accounting department, will be responsible for keeping a close eye on your incoming and outgoing funds, and taking action if and when it looks like you’ll come up short. Most cash flow problems arise when nobody is watching the finances, so if you’re making weekly reports, you should be able to take proactive action before the problem gets any worse.

- Keep a tight leash on purchases. The fewer outgoing expenses you have, the less likely you’ll be to face a cash flow problem. Reducing the number of loans and credit payments you have, as well as restricting purchases, can make your cash go further.

- Conduct credit checks on new customers. Non-payment from customers is a major source of cash flow stress, but you can avoid at least some of this pressure by conducting proactive credit checks on all your customers. You should be able to weed out your biggest threats immediately.

- Perfect your invoicing (and follow up). Iron out your invoicing practices. You should be invoicing customers consistently, in the same ways, and with terms that work in your favor. You also need a documented process for following up with customers who don’t pay you on time (because it will happen eventually). Polite, but firm emails are a good first step, followed by phone calls, then more aggressive action.

- Carefully manage your inventory. Don’t keep more in your inventory than you currently need. Excessive levels of production or storage will be like sequestering cash, rendering it unusable for you. Inventory needs to play a role in your overall cash management.

- Time your outgoing payments. Always pay bills as late as possible. This allows you to keep your cash for the longest period of time, helping you stay positive.

The good news about cash flow is that it’s usually a problem only because of some other fundamental problem in your business, whether it’s a shortage of incoming cash or excessive expenses. It’s entirely in your power to prevent a cash flow problem before it arises—as long as you take it seriously.

This article originally appeared on ValueWalk. Follow ValueWalk on Twitter, Instagram and Facebook.

Yes, you read that right.

If there’s anything the pandemic taught us, it’s that the paradigm of “office” and “workspace” has been shaken to its CORE.

Universities are teaching via Zoom, court dates are done virtually, FULLY REMOTE businesses are valued at $1B+, and legitimate Inc. 5000 startups are run from…wherever. 📲

This is my office for the day…

I am actually running our business from the beach, typing this from here.

It’s 4:28 pm CET, which means it’s 10:28 am EST and I am CRUSHING my to-do list.

(And the team will continue to crush it while I’m asleep. That’s the 🗝)

So how did we get here?

We launched NYCE and our mission to create 100,000 millionaires in March, 2020…just as the global COVID-19 lockdown happened. 😳

As a result, we shut down our main office and set EVERYTHING up to run remotely…

SMOOTHLY! And a system that allows us to outperform competition by 200%. (You can build this system, too. More on this in a second.)

Here’s what we were able to do since then:

- Gained 6M+ followers across all platforms 📈

- Add 1500+ new apartments to the portfolio 🤑

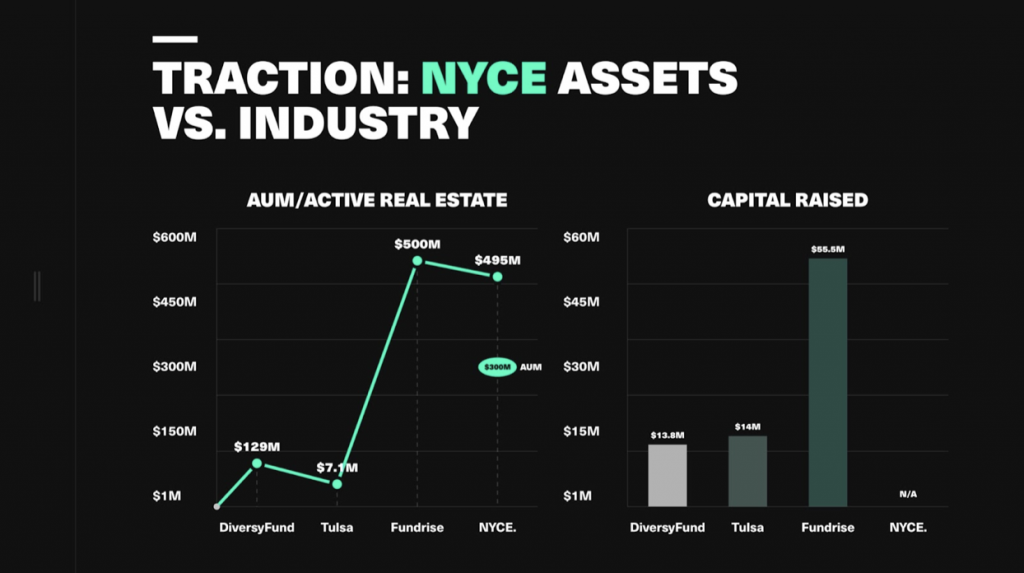

- Grow to $300M in real estate 🚀

- 105% investor returns 🎉

- 700K+ community members 🤝

And here’s the best part…

Having team members in all the main time zones gives us a 24-hour work cycle vs. 9-5/eight-hour on-the-clock performance.

This means we get 3x the productivity of a similar company. 🔥

Let me repeat that…3x PRODUCTIVITY vs. our competitors.

Meanwhile our project management software grants us 24-hour TEAM-WIDE connectivity that tracks all tasks and lets us know if productivity dips even a little bit.

There is ALWAYS someone senior awake. It could be Martin in Barcelona…Nat in New York…Vineet & Arif in New Delhi.

All the while giving YOU GUYS wealth hacks and daily content. 🔥

OK, so how can you do it?!

Well, the first step is to have an actual side hustle you’re launching. Not just an idea, a validated business.

MAJOR KEY: Do NOT spend money until you’ve made your FIRST DOLLAR! 🗝🗝🗝🗝

(You can catch a replay Business Launch masterclass here and see TRIBE member Nessa launched her business on the spot and got her first $45K client shortly after.)

One of the easiest ways to start is with Airbnb—you can start that in 10 minutes. Literally. (Here’s a guide if you need it.)

Once you have your business, you build a virtual infrastructure (you really just need two softwares, which are FREE), manage the team accordingly and run the business from there.

I’m gonna put together a step-by-step video breakdown this weekend inside the new TRIBE U on the FIVE key things you need to do this for YOURSELF. 💵 💎

From what software to use, how to build a team, how to keep.

In the meantime, drop a comment if you’re ready to build some wealth and any questions if you want more…

Let’s get to work. 🙌

PS: If you can’t be bothered with video and just wanna get to work, we’re hosting a TRIBE U workshop that will help you get this process started on the spot. It’s $479 $49. 🔥

Investor and popular Instagram influencer Philip Michael says new fintechs need to take greater responsibility for their younger traders.

“Promoting financial literacy is a must, but encouraging risky gambling is reckless,” Philip Michael, NYCE CEO, says.

In 2020, a 20-year-old Robinhood trader killed himself after engaging in risky options trading and seeing his balance $730,000 in the red, leading to a wrongful death lawsuit against the investment app.

“The main apps onboard as many new users as humanly possible, but there’s really no educational process,” Michael says, “and these first-time investors are left to figure things out on their own.”

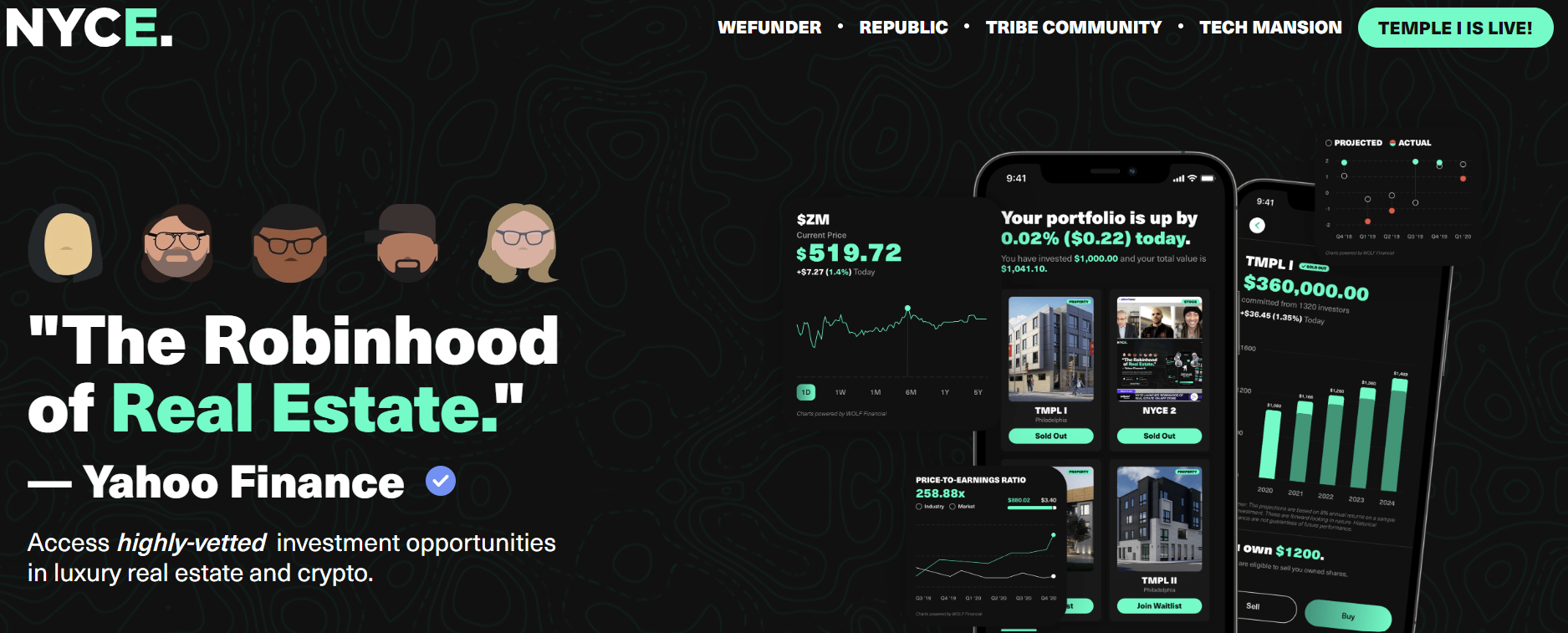

NYCE—a fintech focused on creating wealth for minorities—wants to create 100,000 millionaires through real estate investments and wealth education.

Through its app, investors can own shares in apartment complexes for as little as $100.

Since launching, NYCE has set records for most new first-time BIPOC real estate owners, buying over 1500 apartments in the pandemic and splitting ownership with its investor crowd.

Once investors are in, NYCE automatically enrolls investors in an online wealth academy (TRIBE) that teaches basic wealth principles, responsible investing and how to spot irregular fads like altcoins and meme stocks.

“Becoming a millionaire is a function of time and habit, not luck and one-time scores,” Michael says. “The micro-investments are really just the gateway drug to that wealth mindset.”

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >