Wealth Hacks

Mastering Decision Making: 7 Great Quotes From The Richest Man Alive

“You have to realize: decision making isn’t one size fits all,” said Bezos at a gala this month held in New York by FIRST, a global STEM education nonprofit.

How to make the right decision

You must ask yourself two simple questions: “What are the consequences of this decision?” and “Is this decision reversible?”

“Reversible decisions”

According to Bezos, most decisions are low consequence, reversible. and can be made quickly with data and by junior teams. “If you make the wrong decision,” Bezos explained, “the cost is low.”

Importance of moving fast

Big companies can become less nimble when small, reversible decisions go through cumbersome bureaucratic process. Bezos says moving fast—even if it’s not the best move—still gives you a leg up on the competition.

“The cost of being slow is so much higher than the cost of getting the answer exactly right,” he said.

“Don’t wait”

he said, “Most decisions should probably be made with somewhere around 70 percent of the information you wish you had,” Bezos wrote in a 2016 shareholder letter. “If you wait for 90 percent, in most cases, you’re probably being slow.”

“Irreversible decisions”

Irreversible decisions, Bezos says, are important decisions that should be made by senior leadership, single individuals or tiny teams.

Here, you have “to use very slow, deliberate decision-making processes,” he says. He also calls theses “one-way doors,” in a 2015 shareholder letter.

“If you walk through and don’t like what you see on the other side, you can’t get back to where you were before.”

Intuition matters

“People think of Amazon as very data-oriented and I always tell them, look, if you can make the decision with data, make the decision with data,” he said. “But a lot of the most important decisions simply cannot be made with data.”

Exhibit A: Amazon Prime

“There wasn’t a single financially savvy person who supported the decision to launch Amazon Prime. Zero. Every spreadsheet showed that it was going to be a disaster,” said Bezos. “So that had to just be made with gut.”

“Those kinds of decisions,” added Bezos, “they cannot be made analytically, so far as I know. They have to be made with gut.”

In times of economic uncertainty, gold has long been a reliable investment option for those looking to hedge against inflation and volatility.

If you’re looking to invest in the production of gold, as well as gold itself, here are three stocks you can buy inside the NYCE app today.

1. Barrick Gold Corporation (GOLD)

Barrick Gold Corporation is one of the largest gold mining companies in the world with operations in North America, South America, Africa, and Australia.

Performance: Barrick Gold Corporation has experienced steady growth in the past decade, with its stock price increasing by 31% from 2010 to 2020.

Known for: Barrick Gold Corporation is a leader in responsible mining practices, and is committed to environmental sustainability and social responsibility.

NYCE APP CTA:

2. Newmont Corporation (NEM)

Newmont Corporation is one of the world’s leading gold mining companies with operations in North America, South America, Australia, and Africa.

Performance: Newmont Corporation has experienced significant growth in the past decade, with its stock price increasing by 184% from 2010 to 2020.

Known for: Newmont Corporation has a strong track record of responsible mining, and has been recognized as a leader in environmental stewardship and social responsibility.

3. Franco-Nevada Corporation (FNV)

Franco-Nevada Corporation is a royalty and streaming company that provides financing to gold mining companies in exchange for a share of their future production.

Performance: Franco-Nevada Corporation has experienced substantial growth in the past decade, with its stock price increasing by 780% from 2010 to 2020.

Known for: Franco-Nevada Corporation offers investors exposure to the gold industry without the risks associated with mining operations, making it a popular choice among risk-averse investors.

From selling cookies on the streets of New York to sending personalized messages on potatoes, these five entrepreneurs turned their unconventional ideas into multi-million dollar businesse

- “How a High School Dropout Made $10 Million Playing Video Games Online”

This story is about Matthew Haag, also known as Nadeshot.

Nadeshot. 🤨

He dropped out of high school to pursue a career in gaming and became a professional gamer. He has since won multiple championships and has a large following on social media.

- “Meet the Teen Who Turned His Hobby into a $1 Million E-Commerce Business”

This story is about Cory Nieves, also known as Mr. Cory.

Mr. Cory started a cookie business at the age of six, selling cookies on the streets of New York.

He eventually turned his hobby into a successful e-commerce business, selling cookies online and in stores.

He has been featured on various media outlets and has even baked cookies for Oprah Winfrey.

- “The Surprising Story of the Stay-at-Home Mom Who Made $100K in One Year Blogging About Knitting”

This story is about Sarah Corey, who started a knitting blog called “My Simple Knitting” while staying at home to raise her children.

Her blog became popular and she eventually started selling knitting patterns and products.

She made over $100K in one year from her blog and has since turned her passion for knitting into a successful business.

- “How One Man’s Love for Potatoes Turned into a $5 Million Online Business”

This story is about Alex Craig, who started a website called Potato Parcel where he would send personalized messages on potatoes.

His business gained popularity and he has since expanded into other products, such as potato socks and potato candles.

He has been featured on various media outlets and his business has grown to make millions of dollars in revenue.

- “Pet Rock Creator Gary Dahl Turned a Silly Idea into a Million-Dollar Business”

This story is about Gary Dahl, who famously created and marketed Pet Rocks in the 1970s.

Despite being a seemingly ridiculous idea, the Pet Rock became a massive success, with Dahl selling millions of Pet Rocks and becoming a millionaire in the process.

READ: How This 9-5’er Made Millions Selling Free Rocks In His Spare Time

wealthlab is a platform for hustlers, doers, entrepreneurs and investors to do epic s&%. Our mission is to create 100M new investors worldwide. Join our academy here.*

Don’t miss:

- ‘I work just 2 hours a day’: A 24-year-old who makes $8,000 a month in passive income shares her best business advice

- This 38-year-old makes $160,000 per month in passive income—after losing his job: ‘I work only 5 hours a week now’

- This 33-year-old mom makes $760,000 a year in passive income—and lives on a sailboat: ‘I work just 10 hours a week’

Sign up now: Learn how to retire with $1M with our wealth academy.

Yes, you read that right.

If there’s anything the pandemic taught us, it’s that the paradigm of “office” and “workspace” has been shaken to its CORE.

Universities are teaching via Zoom, court dates are done virtually, FULLY REMOTE businesses are valued at $1B+, and legitimate Inc. 5000 startups are run from…wherever. 📲

This is my office for the day…

I am actually running our business from the beach, typing this from here.

It’s 4:28 pm CET, which means it’s 10:28 am EST and I am CRUSHING my to-do list.

(And the team will continue to crush it while I’m asleep. That’s the 🗝)

So how did we get here?

We launched NYCE and our mission to create 100,000 millionaires in March, 2020…just as the global COVID-19 lockdown happened. 😳

As a result, we shut down our main office and set EVERYTHING up to run remotely…

SMOOTHLY! And a system that allows us to outperform competition by 200%. (You can build this system, too. More on this in a second.)

Here’s what we were able to do since then:

- Gained 6M+ followers across all platforms 📈

- Add 1500+ new apartments to the portfolio 🤑

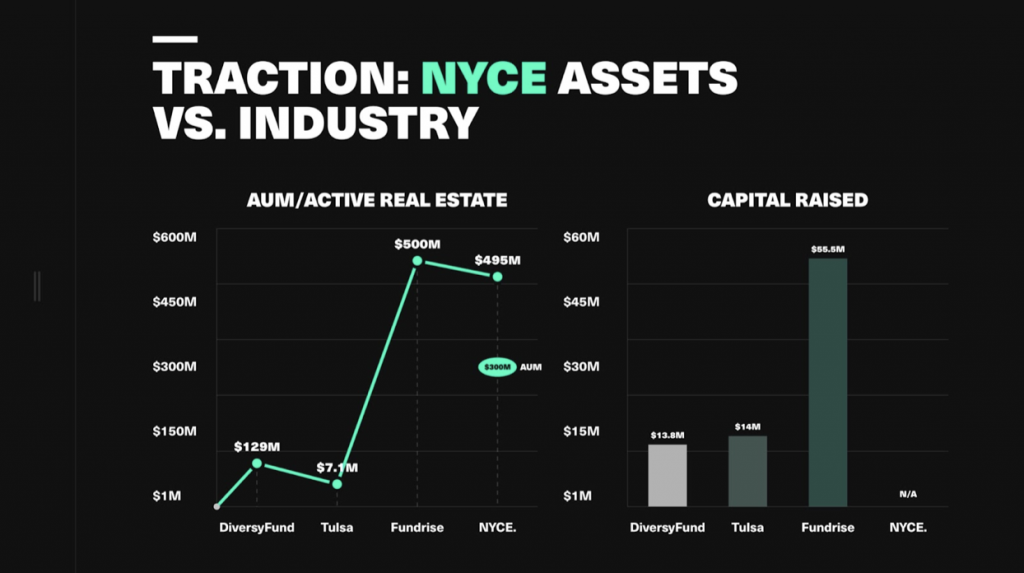

- Grow to $300M in real estate 🚀

- 105% investor returns 🎉

- 700K+ community members 🤝

And here’s the best part…

Having team members in all the main time zones gives us a 24-hour work cycle vs. 9-5/eight-hour on-the-clock performance.

This means we get 3x the productivity of a similar company. 🔥

Let me repeat that…3x PRODUCTIVITY vs. our competitors.

Meanwhile our project management software grants us 24-hour TEAM-WIDE connectivity that tracks all tasks and lets us know if productivity dips even a little bit.

There is ALWAYS someone senior awake. It could be Martin in Barcelona…Nat in New York…Vineet & Arif in New Delhi.

All the while giving YOU GUYS wealth hacks and daily content. 🔥

OK, so how can you do it?!

Well, the first step is to have an actual side hustle you’re launching. Not just an idea, a validated business.

MAJOR KEY: Do NOT spend money until you’ve made your FIRST DOLLAR! 🗝🗝🗝🗝

(You can catch a replay Business Launch masterclass here and see TRIBE member Nessa launched her business on the spot and got her first $45K client shortly after.)

One of the easiest ways to start is with Airbnb—you can start that in 10 minutes. Literally. (Here’s a guide if you need it.)

Once you have your business, you build a virtual infrastructure (you really just need two softwares, which are FREE), manage the team accordingly and run the business from there.

I’m gonna put together a step-by-step video breakdown this weekend inside the new TRIBE U on the FIVE key things you need to do this for YOURSELF. 💵 💎

From what software to use, how to build a team, how to keep.

In the meantime, drop a comment if you’re ready to build some wealth and any questions if you want more…

Let’s get to work. 🙌

PS: If you can’t be bothered with video and just wanna get to work, we’re hosting a TRIBE U workshop that will help you get this process started on the spot. It’s $479 $49. 🔥

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login