Real Estate Investing

These 10 REITs Gained Over 10% In 2018

Real Estate Investment Trusts (REITs) continue to remain popular among investors. Over 90% of REITs have higher dividend yields compared to the average S&P 500 company.

Similar to stocks, REITs need to be held over a long period of time for them to generate substantial returns. Here are 10 REITs that gained 10% in 2018.

1. Arbor Realty Trust [ABR]

Arbor Realty Trust [ABR] is a REIT that engages in the provision of loan origination and servicing across senior housing, healthcare, multifamily, and commercial asset verticals.

ABR has a market cap of $2.4B and has gained over 50% in 2018, primarily driven by robust sales and earnings growth — which no doubt puts a smile on CEO Ivan Kaufman’s face.

Dividend Yield: 9.5%

Total Gain: $800M

CY 2018 Return: 50%

2. Apollo Commercial Real Estate Finance [ARI]

A mortgage REIT, ARI acquires and invests in commercial real estate mortgage loans, subordinate financings, and other real-estate debt instruments. ARI has a market cap of $2.4B and has gained 10.3% in 2018.

Even better, ARI beat analyst estimates in two of the last four quarters.

Dividend Yield: 9.5%

Total Gain: $225M

CY 2018 Return: 10.3%

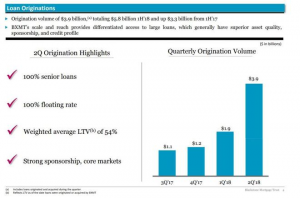

3. Blackstone Mortgage Trust [BXMT]

The Blackstone Mortgage Trust engages in originating senior loans collateralized by commercial real estate. This REIT aims to protect shareholder value and produce risk-adjusted returns through dividends.

BXMT has a market cap of $4B and has gained close to 11% in 2018. The share price has enjoyed an upward climb as BXMT managed to beat earnings estimates coupled with robust revenue growth.

Dividend Yield: 7.2%

Total Gain: $360M

CY 2018 Return: 10.8%

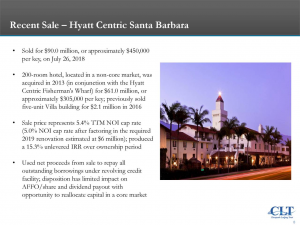

4. Chesapeake Lodging Trust [CHSP]

The Chesapeake Lodging Trust manages and operates hotels. It has an enviable portfolio including The Royal Palm, Hyatt Regency, Le Meridien, JW Marriott, Hotel Adagio, Ace Hotel, Hilton Checkers, Homewood Suites, and Hotel Indigo.

In July 2018, CHSP closed the sale on the Hyatt Centric Santa Barbara which is a 200-room hotel for $90M.

CHSP has a market cap of close to $2B and this REIT has gained 24.2% in 2018.

Dividend Yield: 4.8%

Total Gain: $380M

CY 2018 Return: 24.2%

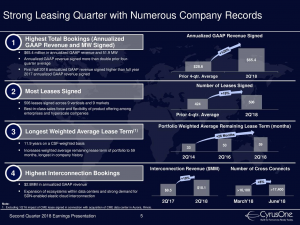

5. CyrusOne [CONE]

CyrusOne owns, develops and operates multi-tenant data center properties. This REIT provides data center facilities to ensure continuous operations of IT infrastructure companies.

CONE has a market cap of $6.4B and has risen 15% in 2018. Last month, CONE closed the $440M purchase of Europe-based Zenium Data Centers. This expansion into Europe is expected to positively impact revenue for CONE.

Analysts expect CONE’s revenue to grow 22.4% in 2018 and 19% in 2019.

Dividend Yield: 2.8%

Total Gain: $830M

CY 2018 Return: 15%

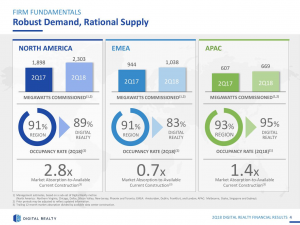

6. Digital Realty Trust [DLR]

Digital Realty Trust owns, acquires and manages technology-related real estate. It provides data centers, colocation, and interconnection solutions. DLR is one of the largest REIT companies with a market cap of $26.4B.

DLR has gained close to 11% in 2018 and is expected to benefit from the global boom in cloud capital spending.

Dividend Yield: 3.3%

Total Gain: $2.4B

CY 2018 Return: 10.9%

7. Education Realty Trust [EDR]

Education Realty Trust focuses on the acquisition and development of housing communities near university campuses.

It has a market cap of $3.3B and has risen 21.5% in 2018. EDR has an impressive earnings history that has driven shares of the REIT upwards. In fact, EDR has beaten earnings estimates by 270% in Q2 2018, 121% in Q1 2018, 28% in Q4 2017 and 80% in Q3 2017.

Dividend Yield: 3.8%

Total Gain: $591M

CY 2018 Return: 21.5%

8. EastGroup Properties [EGP]

EastGroup Properties [EGP] acquires and operates industrial properties in the United States. Its portfolio consists of distribution facilities in Florida, California, Texas, Arizona, and North Carolina.

EGP has a market cap of $3.45B and has risen 11.1% in 2018. Large dividend payouts from REITs continue to entice investors and EGP raised dividends by 12.5% in its latest quarter. EGP has in fact increased dividends for seven consecutive years now.

Dividend Yield: 2.6%

Total Gain: $341M

CY 2018 Return: 11.1%

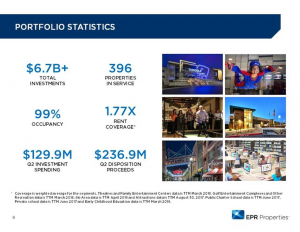

9. EPR Properties [EPR]

EPR Properties is involved in the development and leasing of theatres and entertainment centers. With a market cap of $5.2B, EPS has risen almost 12% in 2018.

EPR’s revenue is estimated to rise 13.3% in 2018 and 5.4% in 2019. The stock is currently trading at $69.84 and the high analyst target estimate for EPR is $71.

Dividend Yield: 6.1%

Total Gain: $552M

CY 2018 Return: 12%

10. Granite Point Mortgage Trust [GPMT]

Granite Point Mortgage Trust focuses on originating, investing and managing senior commercial mortgage loans and other debt, such as commercial real estate investments. GPMT has a market cap of $828M and has risen 12.3% this year.

Similar to other REITs in this list, GPMT has benefitted from encouraging revenue growth in 2018. Analysts expect revenue to rise 24% in 2018 and 18.5% in 2019.

Dividend Yield: 8.3%

Total Gain: $155M

CY 2018 Return: 12.3%

By Sheryl Chapman

As we all know, the economy can be unpredictable at times. Recession is a common phenomenon that can affect the investments in your portfolio.

But don’t worry, there are some sectors that are likely to perform well—even during a recession. Here are five recession-proof investments that you can consider adding to your portfolio.

(Editor’s note***********:************ If you wanna learn how to start investing for retirement, check out the free lessons inside the academy! 📺)*

1. Consumer staples

Consumer staples are products that are essential to our daily lives, such as food, household goods, and personal care items.

These products are in constant demand, regardless of the economic climate. Companies that produce these items, such as Procter & Gamble and Coca-Cola, are considered recession-proof investments.

These companies have a stable revenue stream that can weather economic downturns.

2. Utilities

Utilities are another recession-resistant investment. People need electricity, gas, and water, regardless of the state of the economy.

Utility companies, such as Duke Energy and American Electric Power, have a steady stream of revenue and provide investors with a reliable source of income.

3. Healthcare

The healthcare industry is recession-proof because it provides essential services that people cannot do without. Companies that provide healthcare services or products, such as Johnson & Johnson and UnitedHealth Group, are likely to remain profitable during a recession.

4. Gold

Gold is a safe-haven investment that many investors turn to during times of economic uncertainty. Gold prices tend to rise during recessions because it is seen as a store of value. Investors can buy physical gold, gold ETFs, or invest in gold mining stocks.

GUIDE: 3 Ways To Invest In Gold In 3 Minutes Or Less 🔑📲

5. Treasury bonds

Treasury bonds are considered to be one of the safest investments during a recession.

These bonds are issued by the US government and are backed by the full faith and credit of the government. Treasury bonds provide a fixed income and are considered to be a low-risk investment.

In conclusion, these five investments are considered to be recession-proof because they provide essential products or services that people cannot do without.

Adding these investments to your portfolio can provide stability during times of economic uncertainty.

Airbnb has revolutionized the travel industry by providing an affordable and unique way for travelers to experience different destinations.

With over 7 million listings worldwide, it’s safe to say that Airbnb has become one of the most popular ways for travelers to find lodging.

However, as a host, one of the most challenging decisions you’ll face is determining the right price for your listing.

Pricing your Airbnb listing correctly is critical to your success as a host, as it can make or break your profitability.

Here are some tips to help you price your Airbnb listing for maximum profit:

Know Your Market

Before you set your price, it’s essential to research the market in your area. Look at other listings in your neighborhood, paying attention to the size of the property, amenities, and location. Check the availability of your competitors and the average price they charge. This information will help you determine your pricing strategy and ensure that your listing is competitive.

Consider Seasonal Demand

Seasonal demand plays a significant role in the pricing of your Airbnb listing. During peak seasons, such as holidays, festivals, and major events, you can charge higher rates. Conversely, during low seasons, you’ll need to lower your prices to attract guests. Keep track of events happening in your area and adjust your prices accordingly.

Offer Discounts

Offering discounts is an effective way to attract guests and increase your occupancy rate. Consider offering discounts for extended stays, early bookings, or last-minute reservations. You can also offer discounts to guests who leave a positive review or refer new guests to your listing.

Calculate Your Costs

To ensure that your pricing strategy is profitable, you need to calculate your costs. Take into account expenses such as cleaning fees, utilities, maintenance, and taxes. Factor in your time and effort as well. Your goal is to set a price that will cover all your costs while still allowing you to make a profit.

Be Flexible

Finally, be flexible with your pricing strategy. Test different prices and see how they affect your occupancy rate and profitability. Monitor your competition regularly and adjust your prices accordingly. Remember that the market is constantly changing, and your pricing strategy needs to adapt to stay competitive.

In conclusion, pricing your Airbnb listing for maximum profit is a crucial aspect of your success as a host. By researching your market, considering seasonal demand, offering discounts, calculating your costs, and being flexible, you can set the right price for your listing and maximize your profitability.

Happy hosting!

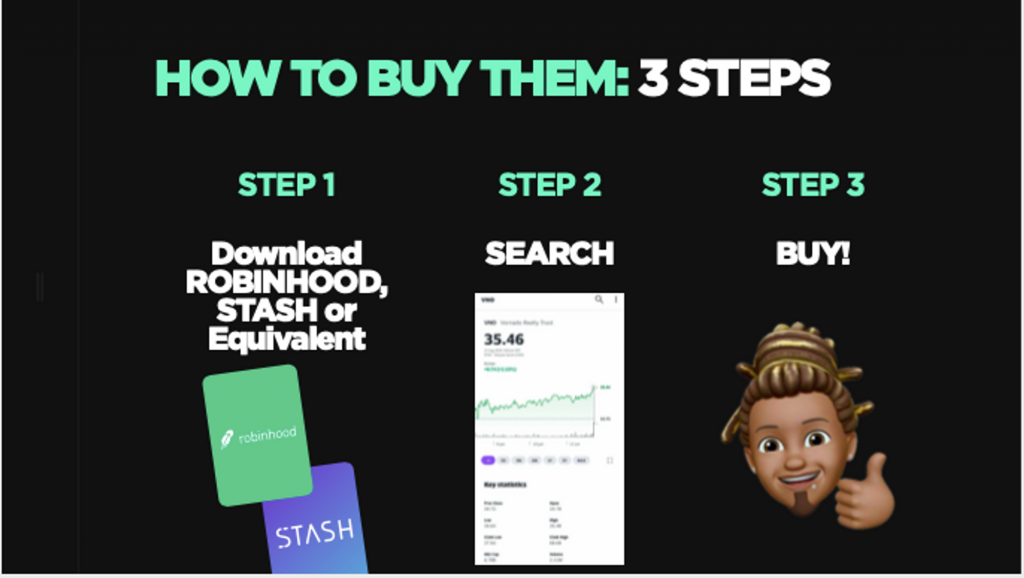

5 REITs that own iconic buildings you can buy today

Real Estate Investment Trusts (REITs) are companies that own and operate income-generating real estate properties.

Investing in REITs has become an increasingly popular way to own a piece of the real estate market without having to buy individual properties.

And you can buy them in the next 5 minutes on the NYCE app…with $5 or less.

Here are five REITs that own iconic buildings across the United States that you can invest in today:

- Empire State Realty Trust, Inc. (ESRT) – ESRT owns the famous Empire State Building in New York City, as well as several other properties in the city.

- Vornado Realty Trust (VNO) – VNO owns the iconic 555 California Street building in San Francisco, which was once the tallest building on the West Coast.

- Boston Properties, Inc. (BXP) – BXP owns several iconic buildings in the United States, including the John Hancock Tower in Boston and the Salesforce Tower in San Francisco.

- SL Green Realty Corp. (SLG) – SLG owns several iconic properties in New York City, including One Vanderbilt, which is currently the fourth-tallest building in the city.

- Macerich Company (MAC) – MAC owns several high-end shopping centers across the United States, including the iconic Santa Monica Place in California.

************************************************************************************************LEARN: How to own real estate with $1000 or less.

Investing in REITs can provide diversification and potentially higher returns than investing in individual properties. However, as with any investment, it is important to do your research and understand the risks involved.

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login