Money

Battle Of The Stocks: Visa Vs Mastercard

In our third edition of the Battle Of The Stocks, we size up two payment processing giants: Visa [V] and Mastercard [MA]. These behemoths account for a majority of the payment processing market share in the United States.

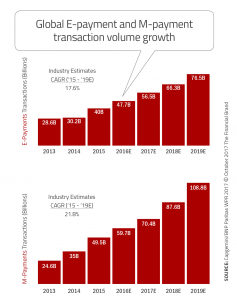

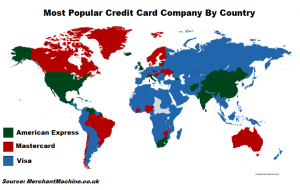

At the end of Q1 2018, Visa was the undisputed domestic leader with a share of 53% followed by Mastercard and American Express [AXP] at 22% each. Visa and Mastercard have benefitted to a large extent driven by the exponential growth in electronic payments.

But historical gains are not an indicator of future performance. Let us look at the key financial metrics between the two companies and compare them to see which is a better buy at current levels.

Market Cap

Driven by the massive increase in share prices, the market cap or market value of Mastercard and Visa have gained significantly over the last few years.

Shares of Visa have risen 220% over the last years and is up 32% in 2018. Comparatively, the Mastercard stock has gained 233% in the last years and 48% in 2018.

Mastercard’s market cap is currently $230.83B while Visa’s market cap is higher at $333B.

Revenue Growth

Revenue growth is a key indicator to gauge the financial position of any company. Any firm that can grow its revenue will be worth investing in. Visa reported sales of 18.36B in 2017. Analysts expect Visa’s revenue to grow 12.2% to $20.6B in 2018 and 11.4% to 23B in 2019.

Mastercard reported sales of $14.95B in 2017. According to analysts, the company is estimated to grow sales by 19.6% in 2018 and 12.9% in 2019.

WINNER: Mastercard

Profitability

The profit margins of payment processing companies are generally high and way above other sectors. The high gross margin translates into robust bottom-lines for companies.

Visa’s operating margin is expected to be 66.5% in 2018 and 68.6% in 2019. Mastercard’s estimated profit margin is lower at 55.8% this year and 57.1% in 2019.

Visa’s estimated net margin is close to 50% in 2018 and 52.3% in 2019. Mastercard, on the other hand, is expected to post a net margin of 43.3% in 2018 and 45% in 2019.

WINNER: Visa

Earnings Growth

While the two companies are looking to improve profit margins, analysts and investors are concerned over the earnings growth potential.

Analysts expect Visa’s earnings per share (or EPS) to grow at 32% in 2018 and 19.1% over the next five years. Comparatively, analysts expect Mastercard’s earnings to rise 40% this year and 22.6% over the next five years.

WINNER: Mastercard

Analyst estimates

We have looked at key financial metrics for the two stocks. Let us now see what Wall Street analysts expect from the two companies. Analysts have a 12-month average target price of $162.18 for Visa, indicating an upside potential of 8.4%.

Comparatively, analysts expect Mastercard’s share price to rise to $231.51, providing an upside potential of 4.1% over the next year.

WINNER: Visa

The scorecard is tied at 2-2. However, we believe that the electronic payments will continue to experience significant growth driven by emerging markets. Mastercard has historically been able to take advantage of foreign opportunities as compared to Visa.

Mastercard also generates substantial fee income from cross-border activities and just pips Visa in this close race. Mastercard was recently added to Goldman Sachs’ [GS] conviction list.

Wealthlab Verdict: Mastercard

Airbnb Experiences: 5 Easy Ways To Make Extra Cash Today

Airbnb is a great way to earn money by renting out your home or apartment.

However, did you know that you can also make money by offering experiences on Airbnb? Here are five easy ways to make extra cash today by creating and offering Airbnb experiences.

1. Offer a food tour

If you love food, why not share your passion with others? Create a food tour experience in your city, showcasing the best local cuisine. You can offer a walking tour or a bike tour, and include stops at local markets, restaurants, and cafes. This is a great way to meet new people and earn money at the same time.

2. Teach a skill or hobby

Do you have a skill or hobby that you’re passionate about? Share your knowledge with others by offering an experience on Airbnb. You can teach anything from photography to cooking to yoga. People are always looking for new experiences, and they’re willing to pay for them.

3. Host a cultural event

If you come from a different culture, why not share it with others? Host a cultural event, such as a traditional dance, music, or art class. This is a great way to showcase your culture and make some extra cash.

4. Offer a nature experience

If you live in a beautiful area, offer a nature experience on Airbnb. You can offer a hiking tour, a kayaking trip, or a birdwatching tour. People love to get out into nature, and they’re willing to pay for it.

5. Host a wellness retreat

If you’re passionate about wellness, why not host a retreat? You can offer yoga classes, meditation sessions, and healthy meals. This is a great way to help people relax and recharge, while earning some extra cash.

In conclusion, offering experiences on Airbnb is a great way to make some extra cash. With these five easy ideas, you can get started today.

For more ideas and tips on how to make money, check out this Airbnb guide inside our academy.

If you’re an Airbnb host looking to increase your revenue, there are several strategies you can implement to make your listing more appealing to potential guests.

Here are 10 tips for making more money with your Airbnb listing:

- Set competitive pricing: Research the prices of similar listings in your area to ensure you’re offering a competitive rate. Consider lowering your prices during slow seasons or offering discounts for longer stays.

- Offer extra amenities: Providing extra amenities, such as a pool, hot tub, or complimentary breakfast, can make your listing more attractive to guests and justify a higher price.

- Invest in high-quality photos: High-quality photos of your space can make a big difference in how many bookings you receive. Consider hiring a professional photographer to capture the best aspects of your listing.

- Keep your listing up to date: Make sure your listing accurately reflects the current state of your property. Update your photos, descriptions, and amenities regularly to keep your listing relevant and appealing.

- Respond promptly to inquiries: Quick responses to guest inquiries can lead to more bookings and positive reviews. Make sure to check your messages frequently and respond as soon as possible.

- Provide excellent customer service: Going above and beyond for your guests can lead to positive reviews and repeat bookings. Make sure to communicate clearly and address any issues promptly.

- Offer local recommendations: Providing guests with recommendations for local restaurants, attractions, and activities can enhance their experience and justify a higher price for your listing.

- Allow instant bookings: Allowing guests to book instantly can make your listing more appealing to those who need to book at the last minute. However, make sure to set clear guidelines for instant bookings to avoid any issues.

- Offer discounts for repeat guests: Offering discounts to guests who have stayed with you in the past can encourage repeat bookings and increase your revenue over time.

- Keep your space clean and well-maintained: A clean and well-maintained space can lead to positive reviews and repeat bookings. Make sure to keep your space clean and address any maintenance issues promptly.

Implementing these 10 tips can help you make more money with your Airbnb listing and improve your overall hosting experience. Happy hosting!

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login