Money

Battle Of The Stocks: Pandora vs. Spotify

(Editor’s note: “Battle Of The Stocks” is a weekly article series where AJ, our resident Wall Street expert, picks two popular stocks in an industry and see how they match up. In this week’s edition, AJ takes a look at two music industry disruptors in Spotify and Pandora.)

We’re nearly a month away from the earnings season, but it’s never too early to gauge performance and scope out stocks with potential to surprise Wall Street and beat estimates.

This time around we compare two publicly traded stocks that are behemoths in the music streaming industry. Who do they match up? Who’s in the lead? And who’s going to take the win?

We’re about to find out. Let’s get ready to rumble.

Pandora vs. Spotify

Pandora [P] and Spotify [SPOT] are global leaders in the music streaming space. There is, however, a difference in the way these companies function.

Spotify members can choose the tracks they want to listen to and when to play them. Pandora is a radio service where users can create a radio station based on their personal choice of music, artists and songs.

While Pandora Premium is available for $9.99 per month and $109.89 annually, Spotify Unlimited is a tad cheaper on the pocket — subscriptions start at $9.99 a month or $99 a year.

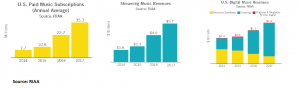

The US music industry has grown from $1.8B in 2014 to $5.7B in 2017. This has unlocked significant opportunities for companies to capitalize on this growth and drive revenue.

Which one is a better stock at current levels? Let’s find out.

Market Value

After going public in early 2011, Pandora has grown to capture a market cap of $2.56B. Pandora’s share price has declined from $13.40 post IPO to its current price of $9.62.

Although the shares touched an all-time high of $37.42 in February 2014, its value has since decreased, eroding massive investor wealth. Surprising many, this year Pandora’s stock is up almost 100%.

On the other hand, Spotify enjoys a much larger market cap of $31.5B. Spotify was publicly listed on April 3, 2018, and closed trading at $149.01. Shares have since risen to its current price of $175.52.

Revenue Growth

Yes, profits are where it’s at. But without revenue, you don’t have much of a business. So which one is raking in more dough?

In 2017, Spotify grossed $4.78B. Spotify’s revenue is expected to grow by 28% year-over-year to $6.12B in fiscal 2018.

By comparison, Pandora grossed $1.47B in 2017 and expects revenue to rise by 5.6% in 2018 to $1.55B, and nearly 12.5% next year.

WINNER: Spotify

Profitability

Spotify and Pandora are still loss-making companies. But with the RIAA (Recording Industry Association of America) highly optimistic about the radio industry, investors will be hoping that the two firms can improve bottom line drastically sooner rather than later.

Moreover, analysts expect Spotify to turn profitable by the end of 2020. Pandora, however, is estimated to report a net loss margin of around 8.4% by 2020.

WINNER: Spotify

Earnings Growth

We’ve seen that Spotify’s profitability is slated to improve at a much higher rate compared to that of Pandora. Spotify’s earnings per share (EPS) is expected to rise 52.5% in 2018 and over 78.5% next year.

Pandora is also expected to improve earnings by 25% this year and around 50% next year, numbers that could cheer investors.

WINNER: Spotify

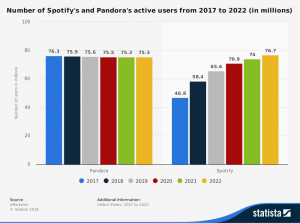

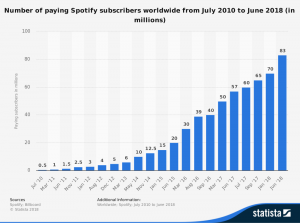

Subscribers

While the above chart shows the active user growth for Pandora and Spotify, we need to consider the number of paid subscribers for both companies.

At the end of Q2 2018, Pandora had just over 6 million paying subscribers. Compare this with Spotify, that has 83 million paid subscribers — Spotify is a strong winner here.

WINNER: Spotify (4-0)

Wealthlab Verdict:

Overall, with a score of 4-0, Spotify wins this battle easily. Though Spotify is a much larger company in terms of market cap, revenue, and subscribers, it is still able to grow sales at a much faster rate compared to Pandora.

A larger subscriber base leads to higher revenue and increased spending for sales and marketing. This results in converting potential customers and is a virtuous cycle that Spotify has taken advantage of.

Airbnb Experiences: 5 Easy Ways To Make Extra Cash Today

Airbnb is a great way to earn money by renting out your home or apartment.

However, did you know that you can also make money by offering experiences on Airbnb? Here are five easy ways to make extra cash today by creating and offering Airbnb experiences.

1. Offer a food tour

If you love food, why not share your passion with others? Create a food tour experience in your city, showcasing the best local cuisine. You can offer a walking tour or a bike tour, and include stops at local markets, restaurants, and cafes. This is a great way to meet new people and earn money at the same time.

2. Teach a skill or hobby

Do you have a skill or hobby that you’re passionate about? Share your knowledge with others by offering an experience on Airbnb. You can teach anything from photography to cooking to yoga. People are always looking for new experiences, and they’re willing to pay for them.

3. Host a cultural event

If you come from a different culture, why not share it with others? Host a cultural event, such as a traditional dance, music, or art class. This is a great way to showcase your culture and make some extra cash.

4. Offer a nature experience

If you live in a beautiful area, offer a nature experience on Airbnb. You can offer a hiking tour, a kayaking trip, or a birdwatching tour. People love to get out into nature, and they’re willing to pay for it.

5. Host a wellness retreat

If you’re passionate about wellness, why not host a retreat? You can offer yoga classes, meditation sessions, and healthy meals. This is a great way to help people relax and recharge, while earning some extra cash.

In conclusion, offering experiences on Airbnb is a great way to make some extra cash. With these five easy ideas, you can get started today.

For more ideas and tips on how to make money, check out this Airbnb guide inside our academy.

If you’re an Airbnb host looking to increase your revenue, there are several strategies you can implement to make your listing more appealing to potential guests.

Here are 10 tips for making more money with your Airbnb listing:

- Set competitive pricing: Research the prices of similar listings in your area to ensure you’re offering a competitive rate. Consider lowering your prices during slow seasons or offering discounts for longer stays.

- Offer extra amenities: Providing extra amenities, such as a pool, hot tub, or complimentary breakfast, can make your listing more attractive to guests and justify a higher price.

- Invest in high-quality photos: High-quality photos of your space can make a big difference in how many bookings you receive. Consider hiring a professional photographer to capture the best aspects of your listing.

- Keep your listing up to date: Make sure your listing accurately reflects the current state of your property. Update your photos, descriptions, and amenities regularly to keep your listing relevant and appealing.

- Respond promptly to inquiries: Quick responses to guest inquiries can lead to more bookings and positive reviews. Make sure to check your messages frequently and respond as soon as possible.

- Provide excellent customer service: Going above and beyond for your guests can lead to positive reviews and repeat bookings. Make sure to communicate clearly and address any issues promptly.

- Offer local recommendations: Providing guests with recommendations for local restaurants, attractions, and activities can enhance their experience and justify a higher price for your listing.

- Allow instant bookings: Allowing guests to book instantly can make your listing more appealing to those who need to book at the last minute. However, make sure to set clear guidelines for instant bookings to avoid any issues.

- Offer discounts for repeat guests: Offering discounts to guests who have stayed with you in the past can encourage repeat bookings and increase your revenue over time.

- Keep your space clean and well-maintained: A clean and well-maintained space can lead to positive reviews and repeat bookings. Make sure to keep your space clean and address any maintenance issues promptly.

Implementing these 10 tips can help you make more money with your Airbnb listing and improve your overall hosting experience. Happy hosting!

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login