Money

This Cybersecurity Stock Gained Over 35% This Year

Cybersecurity stocks are lit this year.

Just as a point of reference, one cybersecurity ETF alone [HACK] is up over 26% in 2018.

You remember the ETFs, right? It’s the investment funds that pick up a type of stock (like tech or REITs), diversify their holdings across that sector, with the idea of giving you nice, solid, stable returns.

Anyway, why are cybersecurities hot?

Pretty simple. As Facebook told the White House a month ago, we’re in a “cybersecurity crisis.”

So basically, as cyber threats continue to increase, so does enterprises spending on cybersecurity.

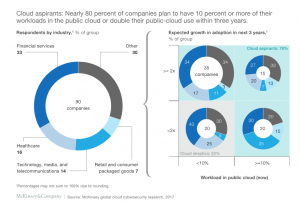

According to McKinsey, almost 80% of companies plan to move 10% or more of their business to the cloud.

So obviously, this mass migration towards the cloud forces increased network security services.

But one in cybersecurity stock, in particular, is straight fire. One of the top cybersecurity companies, Proofpoint [PFPT] has exploded from $4.16B in early January to $6.08B to date.

And the way things are trending, this stock could go even higher. Let’s break it down.

Cybersecurity is growing as a whole

The worldwide security appliance revenue rose 14.3% year-over-year to $3.24B in the first quarter of 2018.

Moreover, the global cybersecurity market is expected to experience serious growth; revenues are expected to explode from $153B in 2018 to $232B in 2022.

Here’s CNBC’s stock expert Jim Cramer breaking down his favorite cybersecurity stocks.

Growth spurt: From $905M to $6B

Proofpoint provides cloud-based security solutions and services, ranging from email protection, ATP (advanced threat protection), data loss prevention, email authentication, secure communication just to name a few.

Shares of Proofpoint have increased over 8x from $14.08 in April 2012 to $119.8 in August 2018, powered by growth in revenue and earnings.

In raw market value, that’s a jump from under $1B in value to more than $6B, as mentioned before. (Sick.)

Revenue’s up 5X

Proofpoint’s revenue has grown from $106M in fiscal year 2012 to $515M as of ’17.

And get this: Analysts expect revenue to continue to climb to $708M in 2018, $906M in 2019 and $1.15B in 2020.

(The cybersecurity crisis must be real!)

Proofpoint’s revenue-driving strategy has historically been focused on new products, acquisitions and partnerships.

(Proofpoint acquired Wombat Security in February 2018. Which followed a 2017 acquisition of Cloudmark, a company specializing in security for messaging services. And Weblife.io, a leader in browser isolation solutions. And…you get the point.)

This strategy—coupled with a high customer renewal rate of over 90%—indicates robust product portfolio and a high customer satisfaction rate.

Still not profitable (but who cares?)

Similar to several other tech companies, Proofpoint is still reporting losses.

That said, Proofpoint’s net margin is expected to improve from -16.8% in 2018 to -10.3% in 2020. As the company continues to gain market share, investors likely won’t care too much either.

The Cali-based company continues to allocate significant resources towards sales and marketing—something analysts expect will impact profit margins in the short-term.

The threats…

There is also a threat of competition from heavyweights like Cisco [CSCO] and other niche players including Palo Alto Networks [PANW], Symantec [SYMC], Fortinet [FTNT] and FireEye [FEYE].

Proofpoint’s shares fell from $127.7 to $112.7 in July after quarterly results were released. Analysts were not too buoyed by the firm’s revenue forecast, which resulted in a sell-off (and thus a drop in the price).

Still all good, though!

All in all, Proofpoint shares have risen 35% in 2018.

The stock seems to have recovered from the Q2 hiccup, too. It rose over 4% on Aug. 24.

That said, the stock is still trading at a discount to its low analyst price target of $125. What does that mean in layman’s terms?

Over 90% of analysts recommend a “buy” on the stock with an average price target of $139.67—plenty of juice left to make a score for the year.

Have at it, WealthLABBERs…

*Opens Robinhood…*

Airbnb Experiences: 5 Easy Ways To Make Extra Cash Today

Airbnb is a great way to earn money by renting out your home or apartment.

However, did you know that you can also make money by offering experiences on Airbnb? Here are five easy ways to make extra cash today by creating and offering Airbnb experiences.

1. Offer a food tour

If you love food, why not share your passion with others? Create a food tour experience in your city, showcasing the best local cuisine. You can offer a walking tour or a bike tour, and include stops at local markets, restaurants, and cafes. This is a great way to meet new people and earn money at the same time.

2. Teach a skill or hobby

Do you have a skill or hobby that you’re passionate about? Share your knowledge with others by offering an experience on Airbnb. You can teach anything from photography to cooking to yoga. People are always looking for new experiences, and they’re willing to pay for them.

3. Host a cultural event

If you come from a different culture, why not share it with others? Host a cultural event, such as a traditional dance, music, or art class. This is a great way to showcase your culture and make some extra cash.

4. Offer a nature experience

If you live in a beautiful area, offer a nature experience on Airbnb. You can offer a hiking tour, a kayaking trip, or a birdwatching tour. People love to get out into nature, and they’re willing to pay for it.

5. Host a wellness retreat

If you’re passionate about wellness, why not host a retreat? You can offer yoga classes, meditation sessions, and healthy meals. This is a great way to help people relax and recharge, while earning some extra cash.

In conclusion, offering experiences on Airbnb is a great way to make some extra cash. With these five easy ideas, you can get started today.

For more ideas and tips on how to make money, check out this Airbnb guide inside our academy.

If you’re an Airbnb host looking to increase your revenue, there are several strategies you can implement to make your listing more appealing to potential guests.

Here are 10 tips for making more money with your Airbnb listing:

- Set competitive pricing: Research the prices of similar listings in your area to ensure you’re offering a competitive rate. Consider lowering your prices during slow seasons or offering discounts for longer stays.

- Offer extra amenities: Providing extra amenities, such as a pool, hot tub, or complimentary breakfast, can make your listing more attractive to guests and justify a higher price.

- Invest in high-quality photos: High-quality photos of your space can make a big difference in how many bookings you receive. Consider hiring a professional photographer to capture the best aspects of your listing.

- Keep your listing up to date: Make sure your listing accurately reflects the current state of your property. Update your photos, descriptions, and amenities regularly to keep your listing relevant and appealing.

- Respond promptly to inquiries: Quick responses to guest inquiries can lead to more bookings and positive reviews. Make sure to check your messages frequently and respond as soon as possible.

- Provide excellent customer service: Going above and beyond for your guests can lead to positive reviews and repeat bookings. Make sure to communicate clearly and address any issues promptly.

- Offer local recommendations: Providing guests with recommendations for local restaurants, attractions, and activities can enhance their experience and justify a higher price for your listing.

- Allow instant bookings: Allowing guests to book instantly can make your listing more appealing to those who need to book at the last minute. However, make sure to set clear guidelines for instant bookings to avoid any issues.

- Offer discounts for repeat guests: Offering discounts to guests who have stayed with you in the past can encourage repeat bookings and increase your revenue over time.

- Keep your space clean and well-maintained: A clean and well-maintained space can lead to positive reviews and repeat bookings. Make sure to keep your space clean and address any maintenance issues promptly.

Implementing these 10 tips can help you make more money with your Airbnb listing and improve your overall hosting experience. Happy hosting!

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login