Business

Uber, Lyft And Top VCs Are Pouring Billions Into ‘Micromobility’—Here’s Why

Nowadays, to Uber somewhere has pretty much become a verb in the English language. But less than 10 years ago, no one even knew what Uber was. And Uber is rumored to be worth $120B on the public markets, should they IPO in the near future.

This might be the reason investors are flocking to bike – and scooter-sharing startups in the so-called “micromobility space.” And at sky high, unicorn-level valuations.

What’s Micromobility?

Micromobility’s an industry tackling “last-mile transportation.” Or in other words, basically that sweet spot between too far to walk, but too short to Uber.

On the heels of the booming ride-sharing industry, new modes of transportations are shooting up. Right now, there are more than 20M dockless bikes in China, electric scooters in Silicon Valley and dockless e-bikes in DC.

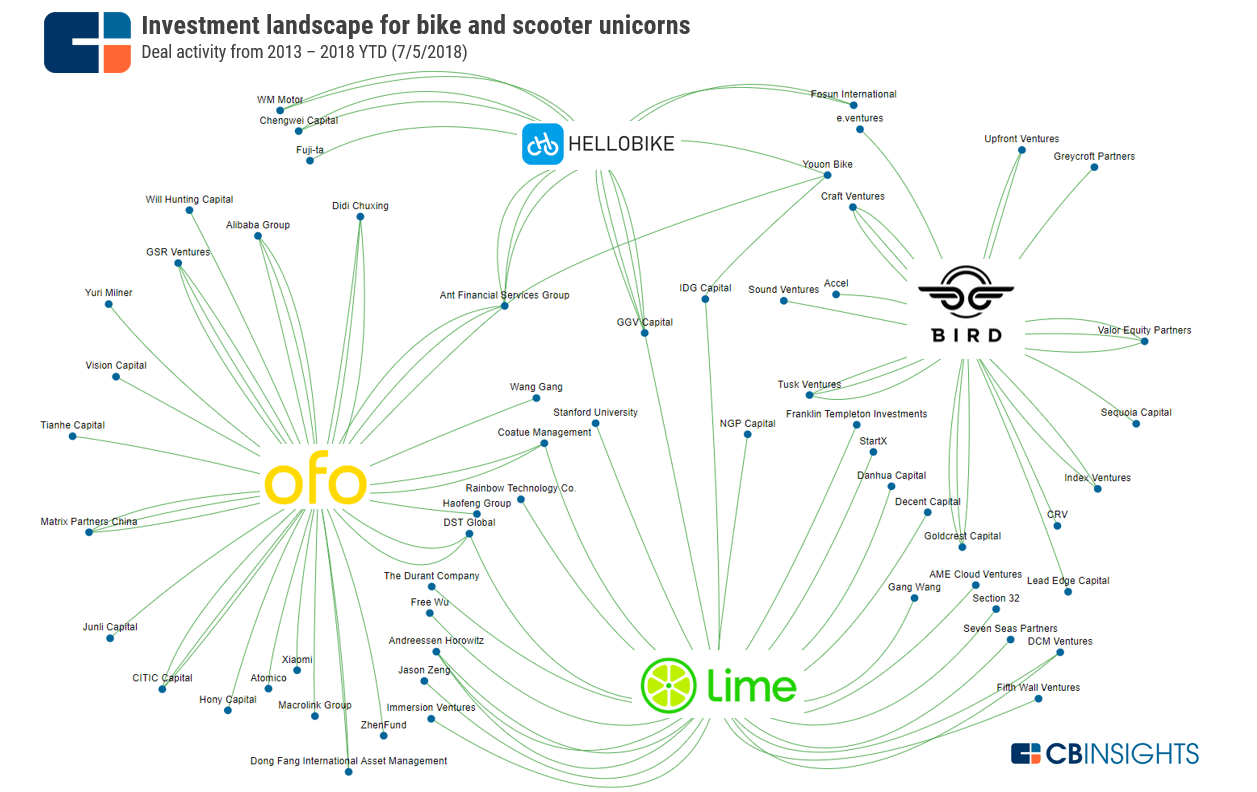

Who are the players?

There are four players in the micromobility space: China-based bike-sharing platforms Ofo and Hellobike, and Bird Rides and Lime, US-based scooter-sharing services. Hellobike, Rides are Lime all attained unicorn status in 2018.

If you can’t beat ’em, join ’em…

At least before they start to beat you. Which is what happened when the arrogant Blockbuster had the chance to own Netflix but instead laughed them out of the room. Or when Uber themselves ate market shares from an ancient, archaic taxi industry.

(On a very serious note, this competition has gotten ugly. NYC cab drivers have been killing themselves, all the while protesting Uber. Although, to be fair, Uber’s been striking deals with taxis in big metros like Moscow to offer their rides through the app.)

But it would appear the ride-sharing giants have taken lessons from these experiences.

In July, Lime just secured a whopping $335M in a Series C funding round led by Google, top VCs and Uber, ironically. Lime declined to reveal their valuation, but Bloomberg reported it at $1.1B. (#Unicorn status, baby.)

That deal in particular indicates the overall bullishness of the micromobility industry, particularly on behalf of the ride-hailing giants. Uber reportedly got in the Lime deal not just for the ROI, but also to start offering scooter rentals through the Uber app itself.

Lyft’s gettin’ it in, too

Lyft, on the other hand, went direct-to-consumer, bypassing a startup to just offering electric scooters directly. Just last month, Lyft rolled out its pilot project in Denver and have since rolled out in Santa Monica and Washington DC.

“Fili-bust a move around DC on a scooter,” Lyft says on their page. (How cute. DC, politics, filibustering? Get it? Ha. Ha.)

:no_upscale()/cdn.vox-cdn.com/uploads/chorus_asset/file/12811853/Lyft_Denver_Scooters.png)

Even though Lyft is getting (and becoming) the direct plug to customers, the Lime deal puts Uber ahead in this game. They’re currently the most downloaded transportation app in the US, by a wide margin at that.

For their part, Lyft says they’ll be working closely with the cities to help them roll out in new markets—including monitoring the Denver rollout closely for any and all negative repercussions.

“This is a new thing,” Caroline Samponaro, head of bike, scooter, and pedestrian policy at Lyft, told The Verge. “They will raise a lot of questions. So we’re going to be very hands-on.”

Regulations? Lobbying?

But here’s where it gets tricky. Uber’s had a lot of issues in certain markets, mainly due to regulations. (Which is why being hands-on may be way to go.)

Uber was forced—or elected, depending on who you ask—to leave Denmark, after “failing to persuade the government to change the law on taxis to accommodate its business model,” CNN reported last year.

And there’s still a lot of lobbying to be done. Despite its massive market, micromobility still hasn’t made it to NYC yet. But that doesn’t seem to worry investors too much.

And let’s face it: before Uber was Uber, Uber had to figure out how to get Uber approved.

Here’s a chart of the investment landscape for bike and scooter unicorns.

Yes, you read that right.

If there’s anything the pandemic taught us, it’s that the paradigm of “office” and “workspace” has been shaken to its CORE.

Universities are teaching via Zoom, court dates are done virtually, FULLY REMOTE businesses are valued at $1B+, and legitimate Inc. 5000 startups are run from…wherever. 📲

This is my office for the day…

I am actually running our business from the beach, typing this from here.

It’s 4:28 pm CET, which means it’s 10:28 am EST and I am CRUSHING my to-do list.

(And the team will continue to crush it while I’m asleep. That’s the 🗝)

So how did we get here?

We launched NYCE and our mission to create 100,000 millionaires in March, 2020…just as the global COVID-19 lockdown happened. 😳

As a result, we shut down our main office and set EVERYTHING up to run remotely…

SMOOTHLY! And a system that allows us to outperform competition by 200%. (You can build this system, too. More on this in a second.)

Here’s what we were able to do since then:

- Gained 6M+ followers across all platforms 📈

- Add 1500+ new apartments to the portfolio 🤑

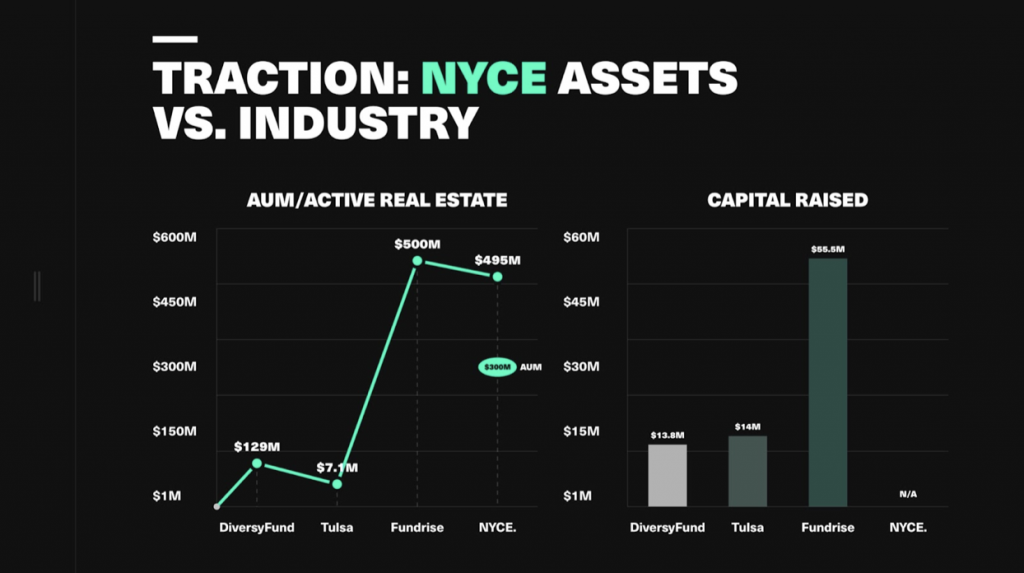

- Grow to $300M in real estate 🚀

- 105% investor returns 🎉

- 700K+ community members 🤝

And here’s the best part…

Having team members in all the main time zones gives us a 24-hour work cycle vs. 9-5/eight-hour on-the-clock performance.

This means we get 3x the productivity of a similar company. 🔥

Let me repeat that…3x PRODUCTIVITY vs. our competitors.

Meanwhile our project management software grants us 24-hour TEAM-WIDE connectivity that tracks all tasks and lets us know if productivity dips even a little bit.

There is ALWAYS someone senior awake. It could be Martin in Barcelona…Nat in New York…Vineet & Arif in New Delhi.

All the while giving YOU GUYS wealth hacks and daily content. 🔥

OK, so how can you do it?!

Well, the first step is to have an actual side hustle you’re launching. Not just an idea, a validated business.

MAJOR KEY: Do NOT spend money until you’ve made your FIRST DOLLAR! 🗝🗝🗝🗝

(You can catch a replay Business Launch masterclass here and see TRIBE member Nessa launched her business on the spot and got her first $45K client shortly after.)

One of the easiest ways to start is with Airbnb—you can start that in 10 minutes. Literally. (Here’s a guide if you need it.)

Once you have your business, you build a virtual infrastructure (you really just need two softwares, which are FREE), manage the team accordingly and run the business from there.

I’m gonna put together a step-by-step video breakdown this weekend inside the new TRIBE U on the FIVE key things you need to do this for YOURSELF. 💵 💎

From what software to use, how to build a team, how to keep.

In the meantime, drop a comment if you’re ready to build some wealth and any questions if you want more…

Let’s get to work. 🙌

PS: If you can’t be bothered with video and just wanna get to work, we’re hosting a TRIBE U workshop that will help you get this process started on the spot. It’s $479 $49. 🔥

Investor and popular Instagram influencer Philip Michael says new fintechs need to take greater responsibility for their younger traders.

“Promoting financial literacy is a must, but encouraging risky gambling is reckless,” Philip Michael, NYCE CEO, says.

In 2020, a 20-year-old Robinhood trader killed himself after engaging in risky options trading and seeing his balance $730,000 in the red, leading to a wrongful death lawsuit against the investment app.

“The main apps onboard as many new users as humanly possible, but there’s really no educational process,” Michael says, “and these first-time investors are left to figure things out on their own.”

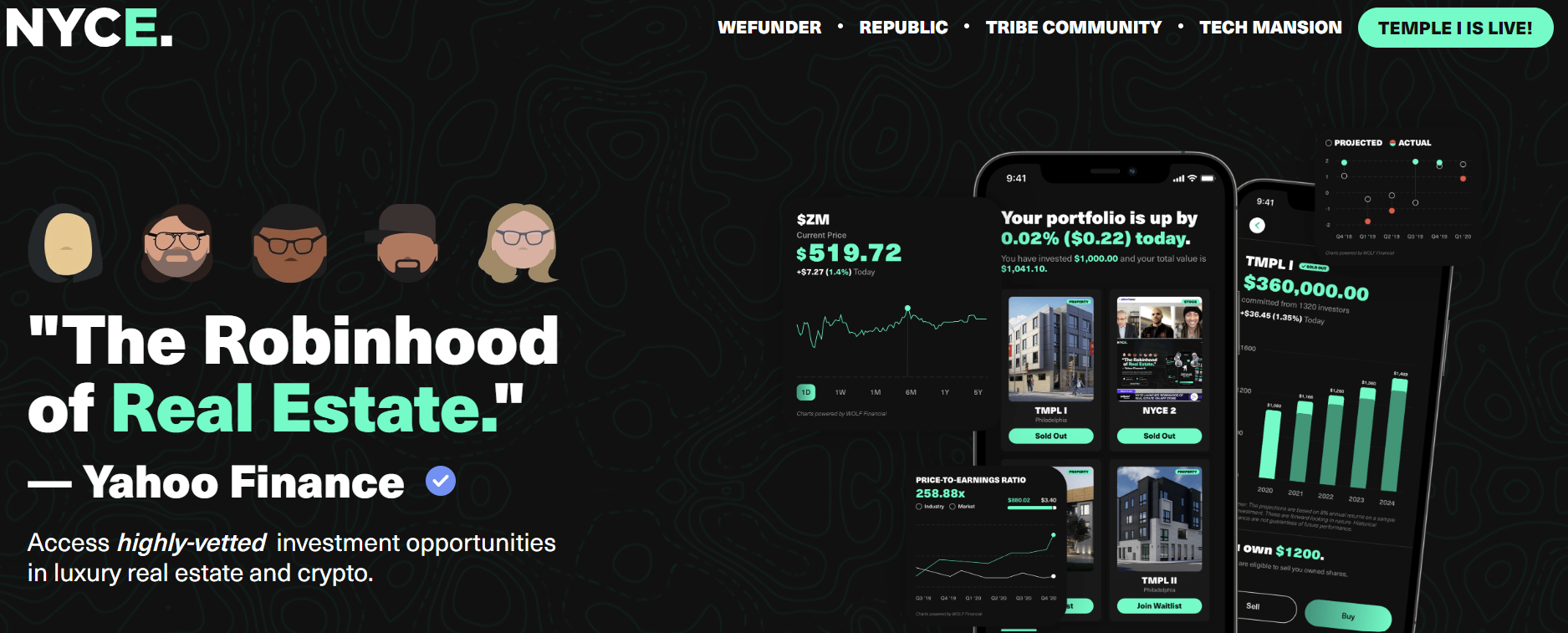

NYCE—a fintech focused on creating wealth for minorities—wants to create 100,000 millionaires through real estate investments and wealth education.

Through its app, investors can own shares in apartment complexes for as little as $100.

Since launching, NYCE has set records for most new first-time BIPOC real estate owners, buying over 1500 apartments in the pandemic and splitting ownership with its investor crowd.

Once investors are in, NYCE automatically enrolls investors in an online wealth academy (TRIBE) that teaches basic wealth principles, responsible investing and how to spot irregular fads like altcoins and meme stocks.

“Becoming a millionaire is a function of time and habit, not luck and one-time scores,” Michael says. “The micro-investments are really just the gateway drug to that wealth mindset.”

Top 5 Best Investment Strategies To Survive A Recession

The Top 10 Investment Opportunities To Capitalize On During A Recession

3 Gold Mining Stocks To Buy Today 📲

You’ve reached your free article limit.

Continue reading by subscribing.

Already a subsciber? Login >

Go back to Homepage >

You must be logged in to post a comment Login